AI in Fintech: How Artificial Intelligence Is Reshaping Finance

Discover how AI in fintech is transforming fraud detection, credit scoring, trading, and compliance. A complete guide to AI applications driving the future of financial services in 2026.

Something fundamental changed in financial services around 2024 — AI stopped being a pilot program and became core infrastructure. The shift wasn’t gradual; it was a step function that separated financial institutions that treated AI as a strategic tool from those that kept it in the experimental sandbox.

The challenge for most organizations isn’t access to AI technology. It’s knowing which applications deliver real operational value, navigating a rapidly tightening regulatory environment, and building governance structures that allow autonomous systems to operate safely at scale.

This guide covers the eight major AI in fintech applications that are reshaping financial services right now, how each technology actually works, and what the regulatory and governance landscape looks like for institutions serious about competing in 2026.

What Is AI in Fintech and Why Does It Matter?

Artificial intelligence in financial technology — or AI in fintech — refers to the application of machine learning, natural language processing, computer vision, and increasingly agentic AI systems to automate, enhance, and reinvent financial workflows. That definition covers a lot of ground, from algorithmic trading systems to conversational banking assistants to autonomous fraud detection engines.

The economic case is straightforward. McKinsey’s research on AI in banking estimates that AI could generate an additional $1 trillion in annual value for the global banking industry — through cost reduction, revenue growth, and risk mitigation. That figure isn’t aspirational. It reflects what leading institutions are already capturing through systematic deployment across fraud prevention, credit decisioning, and operations.

According to Gartner’s 2026 projections, by the end of 2026, 40% of enterprise software will incorporate AI capable of performing end-to-end tasks autonomously — including fraud detection, loan processing, customer onboarding, and reporting — without constant human intervention. That’s not a future state. For the most competitive institutions, it’s already the operating model.

What makes this moment different from earlier AI adoption cycles is the shift from narrow, single-task models to multi-step reasoning systems. Early AI in fintech meant a fraud detection algorithm that flagged suspicious transactions. Today, it means integrated systems that detect fraud, initiate investigation workflows, escalate edge cases, and generate compliance documentation — without human involvement at each step. Understanding that distinction is essential for anyone working in AI in finance broadly or evaluating where to invest AI resources.

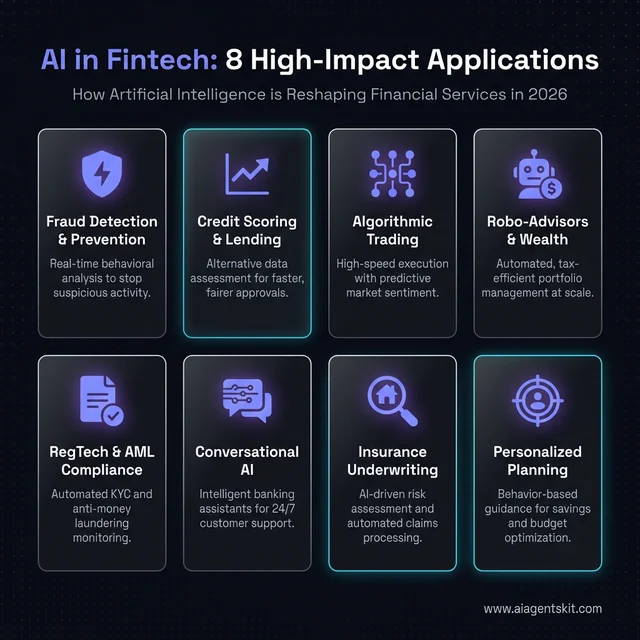

AI in Fintech: 8 High-Impact Applications and Use Cases in 2026.

Generative AI in Financial Services: What Changes and What Doesn’t

Large language models and generative AI have introduced capabilities to financial services that earlier machine learning architectures couldn’t deliver — and financial institutions are moving them from pilot to production faster than any prior AI technology adoption cycle.

The distinction matters. Earlier ML in finance was largely discriminative: models that took structured inputs (transaction amounts, borrower attributes, market prices) and produced structured outputs (fraud score, credit decision, price forecast). Generative AI adds a fundamentally different capability — systems that can reason over unstructured language, generate structured outputs from free-form documents, synthesize analysis from heterogeneous sources, and produce financial-quality written outputs at software speed.

Document Processing and Loan Intelligence

Investment banks and lending institutions process enormous volumes of unstructured documents — loan agreements, regulatory filings, legal contracts, insurance policies — where extracting structured information from free-form text previously required costly specialist review. LLMs now handle this extraction with accuracy approaching specialist human review at a fraction of the cost. JPMorgan Chase’s COIN (Contract Intelligence) program replaced 360,000 hours of annual human loan agreement review with AI processing that completes the same analysis in seconds — with fewer errors, because fatigue-driven mistakes don’t accumulate in model inference the way they do in human reviewers working at volume.

Domain-Specific Financial Models

Bloomberg’s BloombergGPT demonstrated that LLMs trained specifically on financial text outperform general-purpose models on financial NLP tasks. Morgan Stanley built a GPT-4-powered system helping more than 16,000 financial advisors surface relevant research from a library of 100,000+ proprietary documents — redirecting advisor time from information retrieval to client relationships and complex planning. These represent a second-generation deployment model: not general LLM access, but fine-tuned financial models combining language understanding with proprietary institutional knowledge.

Synthetic Data Generation

One of generative AI’s least-discussed applications in finance is synthetic data generation — creating realistic but anonymized transaction datasets for model training, regulatory testing, and product development. Financial institutions frequently can’t use real customer data in development environments due to privacy regulations. Synthetically generated data preserving statistical properties without real PII resolves this constraint, enabling faster model iteration without regulatory exposure.

Quantitative Research Productivity

Generative AI has become genuinely productive for quantitative teams building and maintaining trading models, risk systems, and analytics pipelines. AI coding assistants that understand financial context — domain-specific terminology, standard quant patterns, regulatory constraints — reduce time to develop and backtest quantitative strategies. Banks with large quantitative research teams report meaningful productivity gains: not by replacing researchers, but by eliminating routine coding work previously consuming researcher time better allocated to hypothesis generation.

The investment signal is unambiguous: the global generative AI market in financial services is projected to grow from $1.61 billion in 2024 to $2.17 billion in 2025 — a 35% CAGR placing it among the fastest-growing enterprise technology segments anywhere. That growth rate reflects how quickly institutions are converting from pilots to production deployments across document-intensive, language-heavy workflows where generative AI delivers the most direct and measurable value.

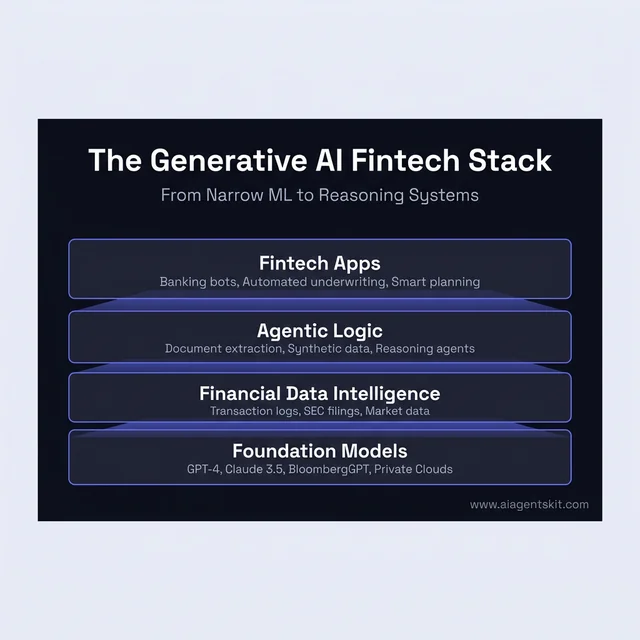

The GenAI Fintech Stack: Moving from narrow ML to multi-step reasoning systems and agentic logic.

8 High-Impact AI Applications Transforming Financial Services

Financial services AI isn’t monolithic. Different application areas have different maturity levels, different risk profiles, and different implementation requirements. Here are the eight domains where AI is delivering the clearest and most measurable impact across the sector:

1. Fraud Detection and Prevention AI-powered fraud detection analyzes real-time transaction patterns, behavioral signals, and device fingerprints to flag suspicious activity in milliseconds. Unlike rule-based systems, ML models adapt continuously to emerging fraud patterns — including deepfakes, synthetic identity fraud, and account takeover attempts sophisticated enough to evade static controls.

2. Credit Scoring and Alternative Lending Machine learning models expand creditworthiness assessment beyond traditional FICO scores to include alternative data: utility payments, e-commerce behavior, cash flow patterns, and mobile transaction history. This enables faster decisions and more accurate risk segmentation across a broader borrower population.

3. Algorithmic Trading and Portfolio Management AI systems execute trades at speeds that were previously impossible for human traders, optimizing order timing, venue selection, and slippage management in response to live liquidity signals. Sentiment analysis using NLP extracts market signals from news, social media, and SEC filings to feed predictive models.

4. Robo-Advisors and Wealth Management Retail and institutional wealth management are both seeing AI integration — from ML-personalized portfolio rebalancing to AI-driven asset allocation. Robo-advisors have moved well beyond simple index strategies into dynamic, goals-based planning that accounts for tax efficiency, life events, and behavioral finance patterns.

5. Regulatory Compliance (RegTech) and AML AI automates Know Your Customer (KYC) identity verification, Anti-Money Laundering (AML) transaction monitoring, and regulatory reporting across complex multi-jurisdictional frameworks. The regulatory compliance AI market — part of the broader RegTech sector — is projected to reach $82.8 billion by 2032.

6. Conversational AI and Customer Service Intelligent banking assistants handle routine inquiries, account management, fraud reporting, and loan intake through natural language interfaces. By 2026, conversational AI is expected to handle 80% of routine customer banking inquiries — freeing human agents for complex, relationship-intensive interactions.

7. Insurance Underwriting and Risk Assessment AI accelerates underwriting through automated document review, real-time risk scoring, and predictive loss modeling. Insurtech companies are using computer vision to assess property damage, telematics data to price auto policies, and NLP to extract risk factors from unstructured documents.

8. Personalized Financial Planning AI analyzes spending patterns, savings behavior, and financial goals to deliver personalized guidance at scale. This extends from budgeting apps to embedded finance tools to institutional advisor platforms — all leveraging machine learning to surface relevant insights at precisely the right moment.

Understanding the breadth of AI agent use cases across industries provides important context for why fintech has become one of the highest-investment domains for AI adoption. The combination of data richness, regulatory pressure to reduce errors, and competitive intensity creates uniquely strong conditions for AI to deliver measurable ROI.

AI in Fintech Use Cases: 10 Real Scenarios Everyone Recognizes

AI in fintech isn’t just an enterprise technology story. It shows up in moments that ordinary people experience every day — often without realizing there’s a machine learning model making a decision in the background. Here are ten real use cases, explained plainly.

1. Your card gets declined while traveling — then a text arrives in seconds

Imagine you’re in Tokyo, and you try to pay for dinner with a card you never use abroad. It gets declined. Then, three seconds later, your bank texts asking if that charge was you. That’s AI fraud detection working in real time — the model spotted that the transaction didn’t fit your pattern and flagged it before it went through. When you confirm it’s legitimate, the system learns from that too. No human reviewed your transaction. The entire sequence happened automatically, in under a second.

2. You apply for a personal loan at 11pm and get approved in 3 minutes

Traditional lending required a loan officer to manually review an application — which meant waiting days or weeks. AI-powered lenders like Upstart, SoFi, and LendingClub use machine learning to analyze thousands of data points (income, spending patterns, employment history, even education signals) and produce a credit decision almost instantly. You fill in a form, submit it, and often have an approval before you’ve finished your tea.

3. Your budgeting app tells you you’re going to overspend this month — before it happens

Apps like YNAB, Cleo, and Copilot don’t just show you what you spent last month. They analyze your income patterns, upcoming recurring bills, and recent spending velocity to predict whether you’re on track — and alert you before you blow past your budget. That forward-looking analysis is machine learning applied to personal finance data. It’s the difference between a rearview mirror and a windshield.

4. Your investment portfolio rebalances automatically after a market dip

You set up a robo-advisor account (Betterment, Wealthfront, or similar) with a target allocation — say, 70% stocks, 30% bonds. When the market drops and your stock allocation falls to 65%, the system detects the drift, calculates the optimal rebalancing trades, accounts for tax implications, and executes them. You didn’t lift a finger. No financial advisor meeting required. The AI handles it continuously, not quarterly.

5. Insurance quote in 60 seconds — no forms, no calls

Modern insurtech apps (Lemonade, Root, Hippo) let you get a home or renters insurance quote in under a minute by answering a handful of questions through a chat interface. In the background, AI cross-references your address with satellite imagery data, public records, and risk databases to generate a real price — not a one-size-fits-all estimate. What used to take three days and a human underwriter now takes less time than ordering coffee.

6. Klarna splits your purchase into four — decided in milliseconds

When you check out on a retailer website and see “Pay in 4 with Klarna,” that option is powered by an AI credit decision that happens in the background while you’re still looking at the checkout page. Klarna’s ML model evaluates your purchase history, credit signals, the merchant category, the cart value, and dozens of other factors to decide whether to offer the installment option and at what terms. If you’ve used it cleanly before, you’ll almost never be declined. The whole underwriting decision takes under 200 milliseconds.

7. A savings app automatically moves money when you won’t miss it

Apps like Chip (UK) and Digit (US) analyze your income deposits, your spending patterns, and your upcoming bills, then quietly move small amounts into savings on days when your balance can handle it without causing an overdraft. The algorithm learns your cash flow rhythm — payday timing, when rent goes out, when you tend to overspend — and optimizes transfers around those constraints. Users consistently report saving more than they would manually because the friction is removed entirely.

8. Your credit card company offers you a limit increase before you ask

If you’ve ever received an unsolicited credit limit increase, it wasn’t a coincidence or good luck. Banks run ML models continuously across their card portfolios to identify customers whose creditworthiness has improved — regular on-time payments, rising income signals, responsible utilization patterns. Proactive increases reduce churn (customers appreciate the trust signal) and increase revenue (higher limits mean more spending). The AI flagged you as worth the upgrade before you even thought to request it.

9. Your bank’s chatbot resolves your dispute without transferring you

When you open a dispute about an unrecognized charge through your banking app, the chatbot that handles your case isn’t working from a script tree — it’s using NLP to understand what you’re describing, pulling your transaction history, cross-referencing known merchant dispute patterns, and in many cases resolving the dispute and issuing a provisional credit automatically. JPMorgan’s internal AI customer service handles millions of customer contacts without human agent involvement. The hold music of banking is quietly disappearing.

10. Opening a new bank account takes 4 minutes instead of 4 days

KYC (Know Your Customer) verification used to require visiting a branch or mailing documents. AI-powered identity verification — the kind used by Monzo, Revolut, Wise, and most modern fintechs — uses computer vision to check your government ID photo against a selfie in real time, verifies document authenticity, runs name and address checks against multiple databases, and flags anomalies in seconds. What took days at a traditional bank now takes the time it takes to take a selfie.

AI in Your Pocket: 6 real-world moments where AI silently powers modern financial convenience.

AI in Fintech Examples: Apps You Already Use (That Are Powered by AI)

The most effective way to understand AI in fintech is to look at products people already use. The following aren’t theoretical deployments — they’re apps actively running AI on millions of users’ financial data right now.

Klarna — AI That Runs Your “Buy Now, Pay Later” Decision

Klarna processes over 2 million transactions per day using AI models that make credit decisions faster than the checkout page loads. The system evaluates each purchase using more than 100 signals — previous purchase history with Klarna, the retailer’s typical risk profile, the item category, time of day, and device behavior patterns. It’s not just asking “can this person repay?” — it’s modeling the probability of repayment for this specific purchase, from this specific person, in this specific context. The sophistication is why Klarna can offer BNPL with minimal defaults while approving the vast majority of transactions instantly.

Cleo — The AI That Roasts Your Spending Habits

Cleo is a UK-born AI financial assistant that connects to your bank accounts and analyzes your spending with a personality. Ask Cleo how your week went financially, and you might get: “You spent £47 at McDonald’s this week. Are you okay?” It’s funny, but there’s serious ML underneath — Cleo categorizes transactions, identifies patterns, predicts upcoming bills, and gives you a “Roast Mode” where the AI delivers genuinely personalized financial feedback based on your actual data. It’s ML-powered behavioral finance made accessible to people who’d never open a spreadsheet.

Lemonade — Insurance Claims Paid in 3 Minutes

Lemonade, the US/EU digital insurance company, uses an AI claims bot called “Jim” that processes insurance claims through a guided video explanation from the claimant. Jim reviews the claim, cross-references it against the policy, checks for fraud signals, and in straightforward cases, approves and pays the claim — sometimes in as little as 3 minutes. The fastest recorded claim payout was 3 seconds. For context, traditional insurance claims take an average of 30 days. The technology running this is computer vision, NLP, and fraud detection ML working together.

Revolut — AI in Your Pocket for 35+ Currencies

Revolut’s multi-currency app uses ML across multiple dimensions simultaneously: fraud detection that flags suspicious transactions in real time, FX rate optimization that identifies the best time to convert currencies, subscription tracking that spots recurring charges you may have forgotten, and spending analytics that categorize every transaction automatically. When Revolut freezes your card for a suspicious transaction at 2am, it’s not a human reviewing your account — it’s a model that spotted a deviation from your spending baseline and acted in milliseconds.

Betterment — Robo-Advisor That Actually Does Financial Planning

Betterment was one of the first robo-advisors, but its current AI goes well beyond simple index fund allocation. The platform uses ML to implement tax-loss harvesting (automatically selling losing positions to offset taxable gains), personalized asset allocation based on your specific goal timelines, and behavioral nudges that trigger during market volatility to keep you from making panic-driven decisions. The documented result: Betterment clients tend to stay invested during downturns and save meaningfully more in taxes than self-directed investors managing similar portfolios.

Credit Karma — AI That Pre-Screens You for Offers

Credit Karma built a business on showing people their credit scores for free — but the real AI product is the offer matching engine. Rather than showing everyone the same credit card and loan offers, Credit Karma uses ML to predict which specific products you’re most likely to be approved for based on your credit profile and financial behavior. The “Approval Odds” feature isn’t a guess — it’s a model trained on actual approval data from partner lenders. For users, it means fewer wasted hard inquiries. For lenders, it means better-qualified applicants.

Plaid — The Invisible AI Infrastructure of Modern Fintech

Most people have never heard of Plaid, but most people who use a budgeting app, a payment app, or a lending platform have used it. Plaid is the data plumbing that connects your bank account to third-party apps when you log in with your banking credentials. The AI layer is in transaction categorization — Plaid’s models process raw transaction data from hundreds of banks (which often comes as generic merchant strings) and translate it into clean, labeled, categorized transaction data. When your budgeting app correctly identifies a charge as “Grocery” instead of “WHOLEFDS MKT #10482,” that’s Plaid’s ML doing the translation work.

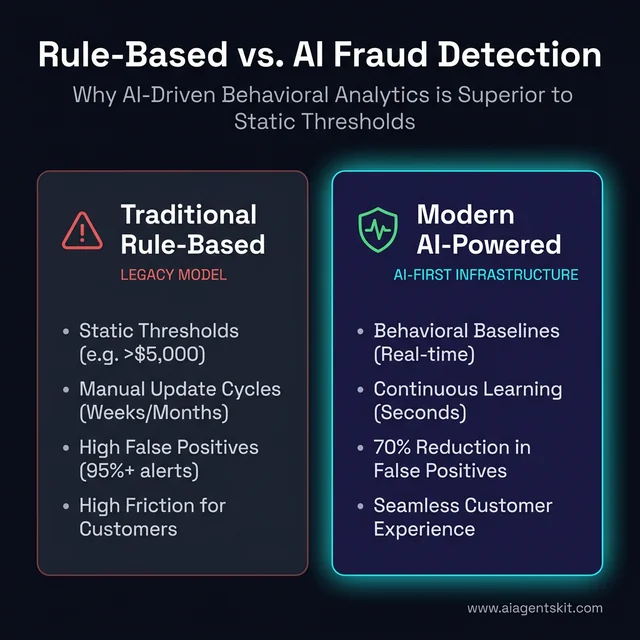

How AI Fraud Detection Keeps Financial Systems Secure

Fraud detection was one of the first fintech applications for machine learning, and it remains one of the most mature. The difference between rule-based fraud systems of the early 2010s and modern AI fraud detection systems is the difference between a static checklist and a continuously learning threat intelligence platform.

The stakes are substantial. AI-powered fraud detection systems are expected to prevent over $25 billion in annual losses across financial services in 2026 — losses that would otherwise flow through to consumers, merchants, and financial institutions through chargebacks, fraud write-offs, and operational overhead.

Traditional fraud systems worked by flagging transactions that exceeded preset thresholds — spend limits, geographic boundaries, transaction frequency. Fraudsters adapted quickly. Modern AI systems take a fundamentally different approach: they model what normal behavior looks like for each individual customer and flag deviations from that baseline, regardless of whether those deviations would trigger a rule-based alert. Understanding the full scope of what AI agents are capable of helps explain why this behavioral modeling approach is so powerful.

Comparison: Why AI-powered behavioral fraud detection outperforms legacy rule-based systems.

Graph Neural Networks and Synthetic Identity Detection

The most sophisticated AI fraud systems now use Graph Neural Networks (GNNs) to build interconnected maps of users, devices, transactions, and accounts. Rather than analyzing each transaction in isolation, GNNs analyze the relationships between entities — the same device being used across multiple accounts, a cluster of accounts with identical attributes, or transaction patterns that trace back to coordinated money movement.

This architecture is particularly effective against synthetic identity fraud — where fraudsters combine real and fabricated information to create fictitious identities that look legitimate in isolation. GNNs can identify synthetic identities by detecting shared attributes (phone numbers, addresses, device fingerprints) across what appear to be separate, legitimate accounts. The network structure that makes synthetic identity fraud lucrative — its distributed, plausible-looking nature — is exactly what GNNs are designed to analyze.

Leading banks and payments companies are also deploying GNNs to map money laundering networks, where complex layering schemes move funds through dozens of entities before reaching their destination. The scale at which these networks can be analyzed — millions of nodes and edges in real time — was impossible with earlier analytical approaches.

How AI Reduces AML False Positives by Up to 70%

The compliance cost of traditional AML systems isn’t just the cost of monitoring. It’s the cost of investigating false positives — and traditional rule-based AML systems generate enormous numbers of them. Industry estimates suggest that between 95% and 99% of AML alerts in traditional systems are false positives, requiring manual investigation time that compliance teams simply don’t have.

AI-driven AML monitoring takes a context-aware approach. Rather than flagging any transaction that exceeds a threshold, ML models assess transactions in the context of the customer’s typical behavior, their industry, their counterparties, and known patterns of legitimate activity. NayaOne’s analysis of AI compliance deployments shows that AI-powered AML monitoring reduces false positives by up to 70% — dramatically reducing compliance operational costs while maintaining or improving detection rates for actual suspicious activity.

That reduction compounds over time as models continue to learn from new data. Organizations that deployed AI-powered AML early are now operating with monitoring systems that are materially more accurate than anything a rule-based approach could achieve — and the operational cost differential continues to grow.

The most advanced deployments combine real-time behavioral analytics with network graph analysis to create layered detection that catches what either approach would miss alone. Teams that operate these integrated systems report substantially improved accuracy at detecting structured layering transactions — the kind of sophisticated money movement that previously slipped through rule-based systems entirely.

AI in Wealth Management: Beyond the First Generation of Robo-Advisors

The first generation of robo-advisors — Betterment, Wealthfront, Schwab Intelligent Portfolios — democratized passive index investing through automated portfolio management. That original model was largely rule-based: assess a risk profile, allocate to a predetermined asset mix, rebalance when drift occurs. Useful, but not meaningfully different in kind from systematic index funds offered through traditional custodians.

AI-powered wealth management in 2026 is categorically different. Machine learning now enables genuinely dynamic, goals-based financial planning that adapts to real-world complexity — tax events, market regime changes, evolving client goals, behavioral finance signals — in ways that static allocation rules cannot.

How ML Transforms Goals-Based Financial Planning

Traditional financial planning optimizes for a single objective — maximize returns for a given risk tolerance — using mean-variance optimization that is backward-looking, sensitive to small input changes, and doesn’t naturally incorporate real client constraints like liquidity needs, tax efficiency, or ESG preferences.

Machine learning enables multi-objective optimization that simultaneously accounts for returns, risk, taxes, liquidity, sustainability criteria, and behavioral patterns. The practical difference: a client with specific university funding goals, a retirement timeline, and ESG constraints receives a dynamically optimized portfolio reflecting all dimensions — updated continuously as market conditions, tax laws, and life circumstances evolve. This isn’t incremental improvement over rule-based robo-advisors. It’s a different category of service.

Tax-Loss Harvesting Automation

AI-driven tax-loss harvesting delivers measurable after-tax return improvement beyond raw portfolio performance. Systems monitoring portfolios continuously — rather than reviewing them quarterly — identify harvesting opportunities that human advisors and scheduled automation miss. Platforms like Wealthfront report 1–2% annual after-tax return improvements through automated harvesting, a figure that compounds substantially over a 20-year wealth accumulation horizon.

Behavioral Finance Integration

ML models analyzing client behavior — how clients respond to drawdowns, decisions they make relative to stated risk tolerance, seasonal patterns — identify clients at risk of making emotionally driven investment decisions before those decisions occur. Proactive outreach triggered by behavioral signals (before a client liquidates at a market bottom) is a concrete category of AI value that rule-based systems fundamentally cannot replicate.

The Human-AI Wealth Advisory Hybrid

Surveys suggest roughly 70% of banking consumers are now comfortable acting on AI-generated financial advice — significantly higher than incumbents anticipated five years ago. But comfort with AI advice doesn’t extend to fully autonomous management for complex, high-stakes decisions like estate planning, business transitions, or major life events.

The model emerging across institutional wealth management is hybrid: AI handles analysis, monitoring, tax optimization, and routine guidance — work consuming advisor time without adding differentiated value. Human advisors focus on relationships, complex planning, and situations where emotional intelligence and accountability genuinely matter. Morgan Stanley’s scale of deployment illustrates this: GPT-4-powered tools actively used by more than 16,000 financial advisors surface research and generate meeting summaries — freeing advisor time for client interaction without removing human judgment from consequential decisions.

Institutional asset management is seeing equally deep AI penetration. UBS uses machine learning to scan trading data and optimize strategies. Finpilot’s AI investment analysis tools have documented 18% higher portfolio returns for users. Hedge funds systematically deploying ML in strategy development demonstrate risk-adjusted return advantages that are difficult to attribute to anything other than superior data integration and model architecture quality.

The Hybrid Wealth Model: Sharing intelligence between autonomous AI engines and strategic human advisors.

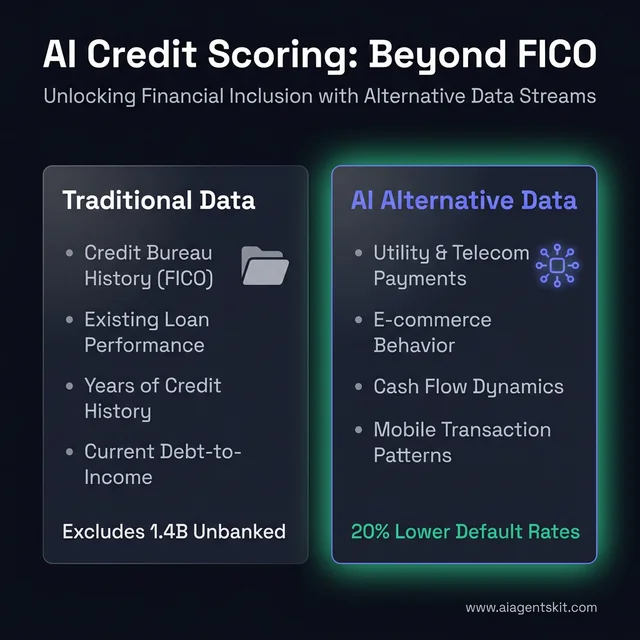

AI Credit Scoring: From Traditional Models to Alternative Data

Credit scoring is experiencing one of the most consequential AI transformations in all of financial services. The traditional model — dominated by FICO scores based on credit bureau data — excluded large segments of the population from affordable credit simply because they didn’t have sufficient credit history, not because they were genuinely poor credit risks.

AI credit scoring doesn’t replace credit history as a signal; it supplements it with a much richer data picture. The implications for measuring AI ROI in credit operations are significant — both in terms of expanded addressable market and reduced default rates on portfolio segments that were previously either excluded or mispriced.

Gartner projects that by 2026, 75% of financial institutions will have implemented AI in credit or lending functions — up from 58% in 2024. That’s a meaningful acceleration, driven by both the competitive pressure to offer faster decisions and the evidence that AI-powered credit models deliver better risk-adjusted outcomes across the full borrower spectrum.

Alternative Data: What AI-Powered Lenders Analyze Today

The categories of alternative data that AI lending models incorporate have expanded rapidly in recent years:

- Utility and telecom payments — rent, gas, electricity, and phone payment history, which reflects financial reliability but rarely appears in traditional credit files

- E-commerce and marketplace behavior — transaction consistency, merchant diversity, return patterns

- Cash flow analysis — income regularity, seasonal patterns, recurring obligations

- Mobile transaction data — frequency, geographic consistency, transaction volume patterns

- Psychometric and behavioral data — in markets where regulators permit, how applicants interact with loan applications

The combination of these signals allows AI models to assess creditworthiness for applicants who would be invisible to traditional FICO-based systems. AI-powered credit models have demonstrated the ability to lower default rates in higher-risk segments by up to 20% compared to traditional models — because they’re capturing risk signals that traditional data simply doesn’t detect.

AI Credit Scoring: Beyond FICO — Leveraging alternative data for financial inclusion and lower defaults.

The speed impact is also significant. Traditional loan underwriting involves manual document review and human decision-making that can take days or weeks. AI automation reduces this to seconds for most standard borrower profiles, with human review reserved for genuinely complex or edge-case applications. AI automation of underwriting workflows is projected to reduce operational costs by 30–50% for lenders that have fully implemented it.

Financial Inclusion and AI Credit Access

The most compelling social dimension of AI credit scoring is financial inclusion. An estimated 1.4 billion adults globally remain unbanked, and hundreds of millions more are underserved by formal financial systems. Most of them aren’t credit risks — they simply don’t have the traditional credit footprint that lenders have historically required.

AI-powered alternative data models can assess these populations based on the financial behavior they do exhibit — mobile money usage, utility payment discipline, business cash flow — rather than requiring a credit history they’ve never had the opportunity to build. The potential to extend affordable credit to gig economy workers, smallholder farmers, informal business owners, and thin-file consumers represents a meaningful structural shift in access to capital.

That said, the risk of algorithmic bias is real and well-documented. If AI models are trained on historical lending data that reflected systemic bias, they can perpetuate or even amplify those biases at scale. The most thoughtful lenders are addressing this through regular fairness audits, development of bias-aware model architectures, and deliberate inclusion of underrepresented populations in model training datasets. Even among experts, there’s genuine debate about the right regulatory and technical approaches to ensuring AI credit systems are both accurate and equitable.

AI in Insurance: How Insurtech Is Rewriting the Underwriting Process

Insurance is the financial services sector where AI is encountering the largest structural inefficiencies — which is precisely why it’s also where the gap between AI-enabled leaders and legacy laggards is widening fastest.

Traditional insurance underwriting is document-heavy, judgment-intensive, and slow. Underwriters review applications, cross-reference risk databases, apply actuarial tables, and produce pricing decisions that can take days for complex risks. AI doesn’t just accelerate that process — it restructures it fundamentally.

Core Pillars: How AI-driven risk assessment and automation are rewriting the insurance industry.

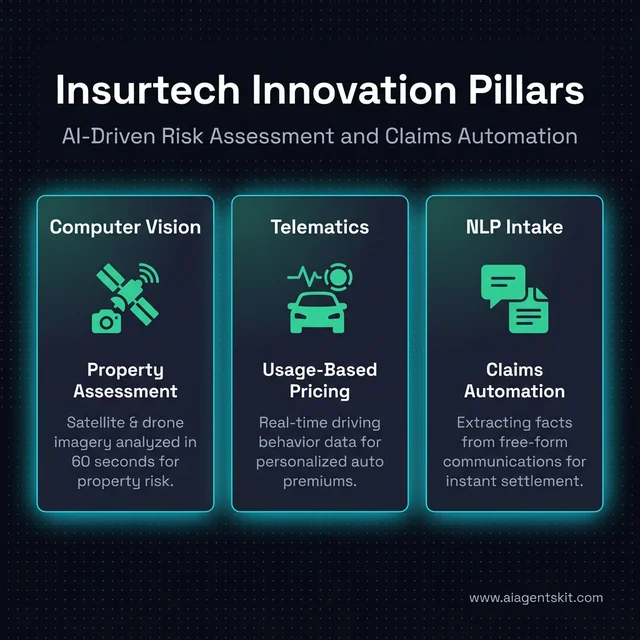

Computer Vision, Telematics, and Claims Automation

Computer Vision for Property Assessment

Insurtech companies now use satellite imagery, aerial photography, and drone footage analyzed through computer vision models to assess property risk without physical inspection. A residential insurer can underwrite a new policy in under 60 seconds by having an AI system analyze publicly available aerial imagery — verifying property characteristics and identifying risk factors like flood zone proximity, roof condition, and tree coverage — for standard risks that previously required physical inspection scheduling and manual review.

After a catastrophe, the same technology dramatically accelerates claims settlement. Rather than waiting for adjusters to visit each damaged property, computer vision models analyze post-event aerial imagery to estimate damage across entire affected regions — prioritizing claims, flagging total losses, and accelerating payouts at a speed no human inspection workflow can match.

Telematics and Usage-Based Insurance

Usage-based insurance (UBI) programs powered by telematics data represent one of the clearest examples of AI enabling a fundamentally more accurate pricing product. Rather than pricing auto insurance on demographic averages, telematics-enabled insurers price based on actual driving behavior: braking patterns, speed consistency, nighttime driving frequency, and mobile device usage while driving. ML models trained on telematics data identify high-risk behavior substantially better than proxy variables like age or neighborhood — and do so in a way that is fairer to individual policyholders who drive carefully regardless of their demographics.

NLP First-Notification-of-Loss Processing

Natural language processing has become a core tool for claims intake. Systems that extract structured information — incident date, location, parties involved, damage description — from free-form claimant communications eliminate the manual data entry step that previously delayed claims workflow initiation. Intake automation typically reduces first-response time from hours or days to under five minutes, with immediate routing to the appropriate handling path.

Embedded Insurance and AI-Powered Risk at Scale

Embedded insurance — financial protection integrated directly into purchase flows and subscription services — is projected to grow 30% in 2025, powered primarily by AI that makes real-time underwriting economically viable at point-of-sale. Consumer electronics device protection at checkout, rideshare driver coverage active only when the app is running, single-flight travel micro-coverage — these products require AI underwriting that assesses risk, prices coverage, and issues a policy in under a second. Human underwriters cannot participate at the necessary speed and cost structure.

The investment landscape confirms where capital is flowing: global insurtech investment reached $5.08 billion in 2025, a 19.5% increase year-over-year, with two-thirds of that funding ($3.35 billion across 227 deals) going specifically to AI-focused insurtechs. That concentration reflects market conviction that AI capability is the primary determinant of sustainable competitive advantage in insurance over the next five years.

What Fintech Regulations Mean for AI Adoption in 2026

The regulatory environment for AI in fintech has shifted from ambiguous to consequential. Regulators in major markets are no longer asking whether AI should be governed — they’re specifying how, with deadlines attached.

The most significant development is the EU AI Act, which entered into force in August 2024. High-risk AI system obligations under the Act — which explicitly include credit scoring, insurance underwriting, and financial risk assessment — hit enforcement dates in August 2026. The EU AI Act obligations for financial services require financial institutions to maintain detailed documentation of AI system logic, establish human oversight mechanisms, conduct conformity assessments, and register high-risk systems with EU regulators.

For fintech companies operating in the EU or serving EU customers, the Act is not aspirational future compliance. It’s current law with active enforcement timelines.

In North America, the picture is developing. Deloitte’s 2025–2026 Regulatory Outlook indicates that US and Canadian regulators will formalize AI governance guidelines requiring financial institutions to demonstrate explainability, auditability, and data provenance for AI systems used in consequential financial decisions.

The broader RegTech market — encompassing all AI tools for compliance automation — is projected to grow to $82.8 billion by 2032, driven largely by the increasing regulatory complexity that makes manual compliance operationally unsustainable. McKinsey and Accenture jointly project that by 2026, more than 70% of financial institutions will deploy agentic and autonomous AI decisioning tools, but specifically under strict governance frameworks — a qualifier that’s reshaping how these systems are being designed from the ground up.

The strategic implication for fintech leaders is that AI governance isn’t a legal overhead cost. It’s a competitive differentiator. Institutions that build explainable, auditable AI systems now will have a structural advantage when regulators tighten requirements — because they won’t be scrambling to retrofit governance onto systems that were built without it.

AI Fintech Companies Leading the Sector: What They’ve Actually Built

Abstract descriptions of AI capability in financial services are far less useful than concrete examples of what institutions have deployed and what they’ve measured. The following cases represent documented, publicly reported implementations.

JPMorgan Chase: 360,000 Hours of Legal Review, Automated

JPMorgan’s Contract Intelligence (COIN) system uses ML to interpret commercial loan agreements — a task that previously consumed approximately 360,000 hours of lawyer and loan officer time annually. The AI system completes the same reviews in seconds, with fewer errors: fatigue-driven mistakes don’t accumulate in model inference the way they do in human reviewers working high volumes of repetitive document review. COIN was not JPMorgan’s first AI initiative, but was the first that produced unmistakable, quantifiable ROI — and that success unlocked broader AI investment across the institution.

Goldman Sachs: 35,000 Hours of Analyst Capacity Recovered

Goldman Sachs’s trading division has integrated AI for execution optimization, order timing, and routing decisions at speeds human traders cannot match. The figure most frequently cited — 35,000 hours of manual analyst work recovered through AI integration — reflects not trading automation itself, but elimination of the analytical preparation work upstream of trading decisions: data aggregation, pattern identification, and scenario construction. That recovered capacity is redirected toward strategy development and complex client work where experienced human judgment adds differentiated value.

PayPal: Real-Time Fraud Scoring at 25 Million Transactions Per Day

PayPal processes roughly 25 million daily transactions, each scored by deep learning models in real time for fraud risk. The models analyze behavioral patterns, device signals, network relationships, and transaction context — continuously improving as new fraud patterns emerge and get incorporated through model updates. The scale illustrates why AI fraud detection has become operationally necessary for large payment processors: no rule-based system could process and score this volume at payment processing latency requirements.

Upstart: 43% More Loan Approvals at the Same Default Rate

Upstart replaced FICO-centric underwriting with ML models incorporating 1,600+ data variables, demonstrating 43% more loan approvals at the same loss rate as traditional models. The mechanism is straightforward: ML captures risk signals that traditional bureau data misses, particularly for consumers with thin credit files who present different actual risk than a FICO score captures.

Feedzai: 60% Fewer False Positives via Generative AI

Feedzai’s generative AI-powered fraud platform documented a 60% reduction in false positives and 20% improvement in fraud detection rates for a major European bank. A 60% false positive reduction translates directly to substantially lower compliance operational costs and materially better experience for legitimate customers incorrectly flagged by legacy systems.

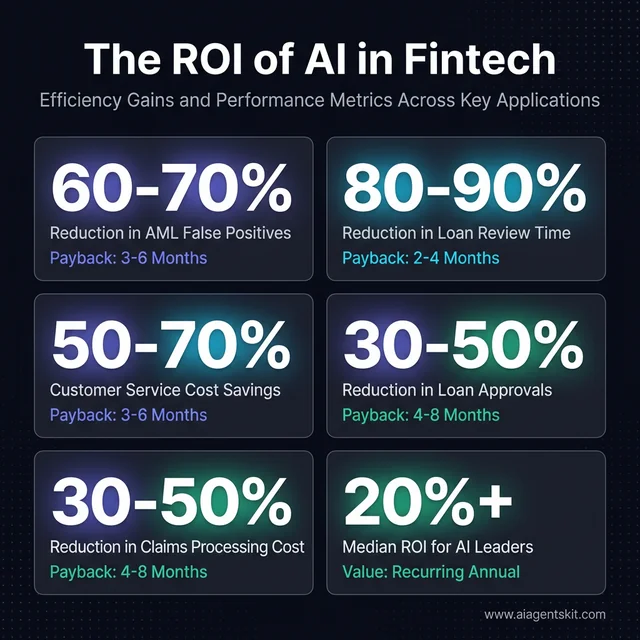

AI Fintech ROI by Application Area

| Application | Typical Impact | Payback Period |

|---|---|---|

| Fraud detection / AML monitoring | 60–70% reduction in false positive costs | 3–6 months |

| Document processing (loan/contract review) | 80–90% reduction in review time | 2–4 months |

| Credit underwriting automation | 30–50% cost reduction per decision | 4–8 months |

| KYC / regulatory compliance automation | 40–60% reduction in compliance ops cost | 6–12 months |

| Customer service automation | 50–70% reduction in tier-1 handling cost | 3–6 months |

| Insurance claims processing | 30–50% faster claim resolution | 4–8 months |

Efficiency & Performance: The ROI and Payback periods for AI applications in fintech.

BCG data shows a median 10% ROI on AI and generative AI investments in financial services, with leaders reporting 20% or more. Nearly 70% of financial services firms report AI driving revenue increases of 5%+, and over 60% report cost reductions of comparable scale. Institutions reporting the weakest returns share a consistent characteristic: they started with overly ambitious first use cases before building the data and governance infrastructure that production AI deployments require.

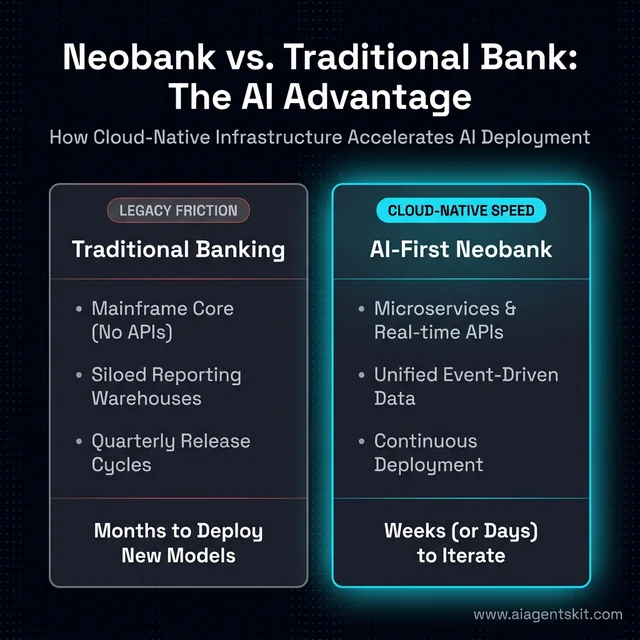

Neobanks and the AI-First Banking Model

The fundamental competitive advantage of digital-native banks isn’t mobile-first design or lower fees — it’s the structural absence of legacy technology infrastructure that creates friction between AI capability and production deployment at incumbent institutions.

A traditional bank deploying AI into its fraud detection system navigates layers of legacy integration: mainframe core banking systems without clean APIs, data warehouses built for reporting rather than real-time inference, and compliance review processes designed for software updates measured in months rather than model updates measured in days. Digital-native neobanks don’t have that friction — and the deployment speed differential is measurable and compounding.

Why Digital-Native Banks Deploy AI Faster

Neobanks like Nubank, Revolut, Monzo, and Chime were built on cloud-native infrastructure with modern data architectures from inception. Every transaction, customer interaction, and product event is structured, logged, and accessible to ML systems in real time. That data architecture advantage explains why neobanks iterate on fraud models, credit models, and personalization systems faster than incumbents with comparable capital resources. Model development cycles measured in weeks — versus the quarters typical in large institutional environments — mean neobanks respond to emerging fraud patterns, new credit signals, and customer behavior changes faster than established competitors.

Nubank’s AI-First Transition at 90 Million Customers

Nubank, Brazil’s largest digital-only bank, has formally transitioned to an “AI-first” business model — developing specialized models for distinct functions rather than deploying generalist AI: dedicated risk models for different product types, ML-driven collections strategies that optimize contact cadence and channel based on individual customer behavior, and personalization models that adapt product recommendations dynamically. At 90+ million customers, the data advantage amplifies model quality in ways that smaller-scale deployments can’t replicate.

Bunq’s Finn: Conversational AI as Core Interface

European neobank Bunq introduced “Finn” — an AI-based conversational interface embedded in the mobile app as a replacement for traditional navigation and search. Finn handles app navigation, transaction queries, financial planning questions, and account management through natural language. The architectural thesis: for mobile-native customers, conversational AI is the natural interface for financial management, not menus or dashboards.

Embedded Finance 2.0: BNPL, Open Banking, and AI Personalization

BNPL products (Klarna, Affirm, Afterpay) require real-time credit decisioning at the point of purchase — in under a second, at scale, without a human underwriter in the loop. The models combine traditional credit signals with behavioral signals (cart composition, purchase timing, merchant category, device characteristics) to make credit decisions both fast and more accurate than traditional subprime credit evaluation. Klarna cited AI as a primary driver of a 40% reduction in operational costs — a figure reflecting how thoroughly AI has permeated its operations beyond just credit scoring.

Open banking frameworks — where customers authorize third-party access to their financial data — provide AI models with precisely the alternative data richness that improves credit and risk assessments for thin-file consumers. Institutions that have built AI systems to consume open banking data operate a compounding advantage: richer data signals drive more accurate models, which deliver better customer outcomes, which build trust, which drives more data sharing authorization. That virtuous cycle is structurally difficult to replicate for institutions that haven’t made open banking-compatible data architecture a strategic priority.

Speed Advantage: How cloud-native neobanks iterate on AI models faster than legacy competitors.

Agentic AI in Banking: The Next Competitive Frontier

Agentic AI represents the most significant shift in how financial institutions can operate — and it represents the front line of competitive differentiation for the next three to five years.

The distinction between conventional AI and agentic AI is function rather than architecture. Conventional AI models analyze inputs and produce outputs — a fraud score, a credit decision, a risk rating. Agentic AI systems act on those outputs. They execute multi-step workflows, interact with external systems, handle contingencies, and complete end-to-end processes without human intervention at each decision point. Understanding how multi-agent systems in financial workflows coordinate activities across different functions helps explain why this capability is architecturally different from single-model AI deployment.

How Agentic AI Systems Operate in Financial Workflows

In practice, agentic AI in banking means systems that don’t just score a loan application — they collect supporting documents, verify employment, assess the property, check regulatory compliance, generate the offer, and initiate the disclosure process. What previously required coordination across multiple specialist teams can execute in minutes, with human involvement triggered only when defined exception conditions are met.

McKinsey and Accenture jointly project that by 2026, more than 70% of financial institutions will have deployed agentic and autonomous AI decisioning tools in at least some operational domain. The domains most advanced in agentic AI deployment include:

- End-to-end loan processing — from application to funding without manual touchpoints for standard profiles

- Account onboarding — KYC, identity verification, account opening, and initial product provisioning

- Regulatory reporting — automated aggregation, calculation, and submission of regulatory filings

- Fraud case management — from detection through investigation documentation to resolution

The Agentic AI Banking Loop: How autonomous agents execute end-to-end financial processes.

The economic case is compelling. Goldman Sachs reportedly saved 35,000 hours of manual analyst work by integrating AI into its trading division — a data point widely cited precisely because it illustrates the order-of-magnitude efficiency gains that agentic approaches can deliver at institutional scale.

Governance Gaps: Why 80% of Banks Aren’t Ready

Here’s the uncomfortable reality about agentic AI in fintech: most institutions deploying it aren’t yet ready to govern it properly.

Deloitte’s State of AI in the Enterprise 2026 report found that only one in five companies currently has a mature governance model for autonomous AI agents, despite the anticipated surge in deployment. That gap — between adoption pace and governance maturity — is where the real risk lies.

The challenge isn’t technical. Agentic AI systems work. The challenge is organizational: defining accountability structures when an AI system makes a bad decision, designing escalation paths that don’t create human oversight bottlenecks, maintaining audit trails that satisfy regulators without degrading system performance, and ensuring that when agentic systems encounter genuinely novel situations, they fail safely rather than catastrophically.

Financial institutions that approach agentic AI deployment with governance infrastructure already in place — defined escalation triggers, circuit breakers, shadow monitoring, explainability requirements — are building competitive systems that can operate at scale. Those treating governance as an afterthought are creating risk that will eventually surface in an operational incident, a regulatory finding, or both.

The recommended architecture for agentic AI in regulated financial environments includes: human-supervised workflows with defined handoff triggers, complete decision logging for regulatory auditability, adversarial testing before deployment, and regular model performance monitoring with automated drift detection. Designing these capabilities into agentic systems from the outset is categorically easier than retrofitting them later.

Regulators have made clear they expect the regulated firm — not the AI vendor — to be accountable for outcomes. That expectation is reshaping procurement decisions, technology design, and how institutions structure AI teams. Organizations that treat AI governance as a compliance checkbox are likely to find themselves at a disadvantage compared to those building it as genuine operational capability.

How to Implement AI in Financial Services: A Practical Framework

The question most financial organizations face isn’t whether AI delivers value — the evidence on that is clear — it’s how to sequence AI investments to generate measurable returns without creating governance liabilities that exceed the efficiency gains.

The organizations seeing the best outcomes have followed a recognizable pattern: start narrow, prove ROI, expand systematically, and build governance infrastructure in parallel with capability development rather than after an incident forces it.

Use Case Selection: Where to Start

Not every financial workflow is equally suited to AI deployment. The highest-ROI starting points share four characteristics:

- High volume — the workflow handles hundreds or thousands of instances per day

- Variable inputs — the task requires processing unstructured or variable inputs that rule-based automation can’t handle reliably

- Measurable outcomes — there’s a clear metric that proves whether the AI outperforms the status quo

- Defined risk tolerance — errors are either recoverable or have defined escalation paths

Most financial institutions find that fraud detection, document processing, and customer inquiry handling score highest on all four criteria — which explains why these three consistently represent the starting point for AI adoption regardless of institution size or type.

Large Banks and Insurance Companies: The highest-priority first deployment is typically AML/KYC automation: high transaction volume, well-defined success metrics (false positive rate, SAR quality), and built-in organizational urgency from compliance requirements. Document processing — loan agreements, contracts, regulatory filings — is the consistent secondary priority where LLM-based extraction delivers unambiguous ROI at scale.

Community Banks and Credit Unions: The practical starting point is customer service automation — a conversational AI system handling routine inquiries (balance checks, rate questions, account restrictions) that reduces staff time on low-value interactions without requiring deep ML infrastructure. This can deploy on existing infrastructure in months, not years.

Fintech Startups: Build ML into the core product function from inception rather than treating it as an enhancement layer. For a lending fintech, that’s alternative data credit scoring. For a payments company, it’s fraud detection. Retrofitting ML into a product architecture built without it is significantly harder than designing with ML-native data flows from the start.

Build, Buy, or Partner: The Implementation Decision

Three options exist: build proprietary models, buy pre-built AI solutions from established vendors (Feedzai for fraud, Upstart for credit), or partner with AI infrastructure providers (Google Vertex AI, AWS Bedrock, Azure AI Studio) to build on foundation models.

The build decision makes sense when: the institution has unique proprietary data providing competitive advantage when used to train models, the workflow is sufficiently distinctive that off-the-shelf solutions don’t fit, and engineering capacity exists to build and maintain production ML systems. The buy decision makes sense when speed to deployment matters most and vendor solutions are proven for the use case. The partner decision — increasingly common — combines frontier model capability with the institution’s proprietary data and workflow integration expertise.

Common Mistakes to Avoid

Underestimating data readiness. AI models are only as good as their training data. Financial institutions frequently discover mid-project that historical data is incomplete, inconsistently formatted, or contains historical biases that will be amplified by the model. A data readiness audit before model development — not concurrent with it — prevents the most common cause of failed AI deployments.

Treating governance as post-deployment. Institutions that have had to recall or suspend AI systems after operational incidents almost universally built governance as an afterthought. Defining accountability structures, audit logging requirements, and human override protocols before deployment — not after a problem surfaces — is categorically easier and cheaper.

Starting with the wrong use case. The temptation to begin with highest-potential applications frequently leads to multi-year projects that don’t produce measurable ROI before organizational patience expires. The better pattern: start with a narrow use case that can be measured and pointed to as evidence of AI’s value within 3–6 months, then expand.

AI in Fintech: Frequently Asked Questions

What is AI in fintech and how does it work?

AI in fintech applies machine learning, natural language processing, and increasingly agentic AI systems to automate and enhance financial workflows. Rather than following predefined rules, these systems learn patterns from historical data and adapt to new information. Applications range from fraud detection models that analyze transaction behavior in real time to autonomous agents that process loan applications end-to-end without human intervention at each step.

How does AI improve fraud detection accuracy in financial services?

AI fraud detection analyzes behavioral patterns, transaction context, device signals, and relationship networks simultaneously — rather than checking transactions against static rules. Machine learning models learn what normal looks like for each customer and flag deviations in real time. Graph Neural Networks detect coordinated fraud schemes by mapping entity relationships across accounts and devices. The result is dramatically lower false positive rates and faster detection of novel fraud types that rule-based systems would miss entirely.

How does AI improve credit scoring accuracy?

AI credit models incorporate alternative data — utility payments, cash flow patterns, e-commerce behavior, and mobile transaction history — alongside traditional credit bureau data. This expands the signal set for creditworthiness assessments, enabling more accurate risk segmentation across the full borrower population. Organizations using AI-powered credit scoring have demonstrated up to 20% lower default rates in high-risk lending segments compared to traditional FICO-based models.

Will AI replace human financial advisors completely?

Surveys suggest roughly 70% of banking consumers are now comfortable acting on AI-generated financial advice — a figure higher than most incumbents anticipated. That said, fully autonomous financial advice for complex, high-stakes decisions remains a regulatory and trust challenge. The more likely trajectory is hybrid models where AI handles analysis, monitoring, and routine guidance, while human advisors focus on relationship management, complex planning, and situations requiring genuine judgment and accountability.

What is RegTech and how does AI power it?

RegTech (Regulatory Technology) refers to technology solutions that help financial institutions meet compliance obligations — including KYC, AML, GDPR, and reporting requirements. AI powers RegTech by automating transaction monitoring, extracting risk signals from unstructured documents using NLP, predicting compliance breaches before they occur, and generating regulatory reports autonomously. AI-powered AML systems have demonstrated a 70% reduction in false positive alerts, dramatically reducing the operational cost of compliance programs.

How does agentic AI work in banking workflows?

Agentic AI systems don’t just analyze data — they execute multi-step processes autonomously. In banking, an agentic AI might receive a loan application, collect required documents, run identity verification, assess creditworthiness, check regulatory compliance, generate the offer letter, and initiate disclosure workflows — all without human involvement for standard cases. Human review is triggered only by defined exception conditions. This approach can compress multi-day processes into minutes while maintaining compliance and audit trail requirements.

What are the biggest challenges of AI adoption in fintech?

The most common friction points are organizational rather than technical: integrating AI with legacy infrastructure, building governance structures for autonomous systems, managing algorithmic bias in credit and underwriting models, and keeping pace with a rapidly evolving regulatory environment. Data quality is also a persistent challenge — AI models are only as good as the data they’re trained on, and financial data often contains gaps, inconsistencies, and historical biases that require careful management before model training.

How does AI promote financial inclusion for the unbanked?

AI credit models can assess creditworthiness for individuals without traditional credit histories by analyzing alternative data — mobile money behavior, utility payment records, business cash flow — that reflects financial reliability without requiring a formal credit file. This enables affordable credit access for gig economy workers, informal business owners, and the estimated 1.4 billion unbanked adults globally who are excluded from traditional financial systems. The caveat: AI systems trained on biased historical data can replicate or amplify existing exclusion patterns, making fairness auditing a critical governance requirement.

What does the EU AI Act require from fintech companies?

The EU AI Act classifies AI systems used in credit scoring, insurance underwriting, and financial risk assessment as high-risk systems. Fintech companies operating in or serving the EU market must: maintain detailed documentation of AI system logic and training data, conduct conformity assessments before deployment, register high-risk systems with EU authorities, implement human oversight mechanisms, and ensure systems are explainable and auditable. High-risk system obligations entered enforcement in August 2026, making compliance an immediate operational requirement.

What is the ROI of AI implementation in financial services?

ROI varies significantly by application area. Fraud detection typically shows the fastest payback through direct loss prevention and reduced false positive investigation costs. AML compliance automation delivers ROI through headcount efficiency — AI can monitor orders of magnitude more transactions than human analysts at lower cost. Credit scoring AI delivers ROI through expanded addressable market, reduced defaults, and faster decisioning. Goldman Sachs’s reported 35,000 hours of saved analyst time illustrates how AI productivity gains compound across large institutions.

What is generative AI in banking and how is it being used?

Generative AI in banking refers to the application of large language models and generative models to financial workflows involving unstructured language — understanding, processing, and producing text-based outputs. Current production deployments include document intelligence (extracting structured data from loan agreements, contracts, and regulatory filings), financial research synthesis, synthetic data generation for model training and regulatory testing, and AI advisory tools that surface relevant research for wealth management professionals. JPMorgan’s COIN system, Morgan Stanley’s GPT-4-powered advisor platform, and Bloomberg GPT represent documented deployments that have proven the ROI case for broader institutional adoption.

How are neobanks using AI differently from traditional banks?

Neobanks have a structural deployment advantage: cloud-native infrastructure with modern data architectures from inception means AI systems access clean, real-time data without the legacy integration challenges slowing AI deployment at traditional institutions. Digital-native banks like Nubank, Revolut, and Bunq operate ML models across fraud detection, credit risk, customer personalization, and product recommendations with iteration cycles measured in weeks rather than the months typical in large institutional environments. The organizational difference is equally significant — AI at neobanks is a core product function, not a separate technology initiative. Nubank’s formal transition to an “AI-first” business model at 90+ million customers illustrates how far this architectural advantage can compound.

What is embedded finance and how does AI make it work?

Embedded finance refers to financial services — payments, credit, insurance, investment — integrated directly into non-financial platforms and purchase flows. AI makes embedded finance economically viable by enabling real-time underwriting and risk assessment at the latency and cost that point-of-purchase financial services require. BNPL credit decisions, travel insurance bundled into a flight booking, and device protection offered at checkout all require credit or risk decisions in under a second. AI-powered underwriting makes this technically and economically feasible; human underwriters cannot participate in these workflows at the required speed or cost structure.

What is the typical ROI of AI investment in financial services?

Research from BCG shows a median 10% ROI on AI and generative AI investments in financial services, with the top quartile of institutions reporting 20% or more. Nearly 70% of financial services firms report AI-driven revenue increases of 5% or more; over 60% report cost reductions of comparable scale. Application-specific payback periods range from 2–4 months for document processing to 6–12 months for regulatory compliance automation. The most consistently cited ROI driver is process cost reduction through automation, though competitive differentiation in fraud prevention and credit risk accuracy is increasingly cited as an equally important strategic return for institutions measuring total impact.

Conclusion

Financial services AI has crossed an inflection point. The institutions seeing the most significant returns aren’t those that deployed the most sophisticated models — they’re the ones that deployed systematically, with clear use cases, appropriate governance, and organizational capacity to act on AI outputs.

The evidence strongly suggests that the next competitive wave won’t be about whether to deploy AI for fraud detection, credit scoring, or operational efficiency. Those decisions have already been made across the industry. The differentiation will come from how well organizations govern autonomous systems, integrate AI into regulatory compliance workflows, and deploy agentic capabilities with the governance infrastructure that allows them to operate safely at scale.

For financial organizations looking to benchmark their AI maturity and build deployment roadmaps across lending, compliance, and operations, the patterns documented in AI for accounting firms and professional services offer relevant context on how professional services organizations are structuring AI adoption — with lessons applicable across the broader financial services landscape.

The technical capability exists. The regulatory frameworks are clarifying. The remaining variable is organizational will — and that’s always been the real constraint on intelligent technology adoption.