AI for Accounting Firms: Complete Automation Guide (2026)

Explore the best accounting ai software tools today. Discover how progressive CPA firms are using hybrid AI automation to scale their operations securely in 2026.

Last month, I was at a partner retreat when someone asked a simple question: “Are we charging too little, or are we just too slow?”

For decades, the traditional CPA firm has been built on manual data entry and the steady accumulation of billable hours. We dedicated the majority of our time to discovering discrepancies in bank feeds and manually rolling forward depreciation schedules.

However, manual data entry is no longer a viable business model. The accounting sector is concurrently facing an unprecedented talent shortage, with the AICPA’s latest Trends Report citing a sharp 7.8% drop in accounting graduates.

To survive in this constrained environment, progressive firms are aggressively deploying advanced accounting AI software. By shifting mechanical operations to intelligent systems, firms solve the talent shortage and elevate their workforce to focus exclusively on high-margin advisory services.

Let’s break down exactly what this transformation looks like, the specific use cases driving the highest ROI, and the exact steps leadership must take to implement change management safely.

The State of AI in Accounting: Unignorable Statistics

If you are still on the fence about whether AI is a passing trend or an industry-wide pivot, the data is entirely conclusive. The world’s largest financial firms and tech analysts have already clearly charted the timeline.

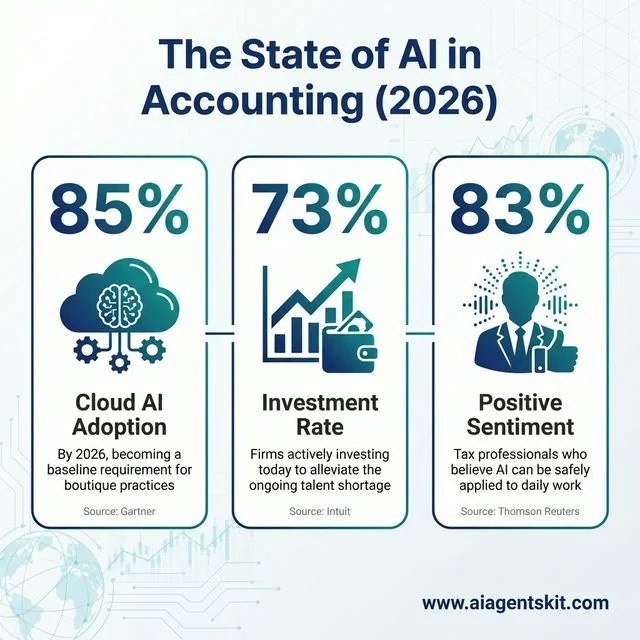

- 85% Cloud AI Adoption: According to Gartner’s latest financial technology projections, 85% of accounting firms will use cloud-based AI-enhanced accounting software by 2026. This adoption is no longer limited to the Big Four enterprise environments; it’s practically a baseline requirement for boutique practices.

- 73% Investment Rate: A recent industry survey by Intuit revealed that 73% of accounting firms are actively investing in AI today specifically to alleviate the ongoing talent shortage.

- 83% Positive Sentiment: Research from Thomson Reuters shows that 83% of tax professionals now believe AI can be safely applied to their daily work. This is a massive structural shift from the heavy skepticism seen just two years ago.

These statistics prove that holding out on AI isn’t simply a matter of preference. It’s an active decision to willingly operate at a severe competitive disadvantage.

The State of AI in Accounting (2026): A statistical infographic highlighting the rapid enterprise adoption timeline across the financial software landscape. According to Gartner, 85% of accounting firms are projected to integrate cloud-based AI tools by 2026, marking a shift where these systems become baseline requirements rather than niche advantages. Intuit’s recent industry survey indicates a massive 73% current investment rate as firm partners actively deploy AI specifically to alleviate the ongoing CPA talent shortage and staffing gaps. Simultaneously, Thomson Reuters research reveals an 83% positive sentiment marker, proving that tax professionals now believe machine learning models can be safely and securely applied to their complex daily workflows. These statistics conclusively prove that embracing sophisticated structural automation is no longer optional for firms expecting to remain competitive.

The State of AI in Accounting (2026): A statistical infographic highlighting the rapid enterprise adoption timeline across the financial software landscape. According to Gartner, 85% of accounting firms are projected to integrate cloud-based AI tools by 2026, marking a shift where these systems become baseline requirements rather than niche advantages. Intuit’s recent industry survey indicates a massive 73% current investment rate as firm partners actively deploy AI specifically to alleviate the ongoing CPA talent shortage and staffing gaps. Simultaneously, Thomson Reuters research reveals an 83% positive sentiment marker, proving that tax professionals now believe machine learning models can be safely and securely applied to their complex daily workflows. These statistics conclusively prove that embracing sophisticated structural automation is no longer optional for firms expecting to remain competitive.

What is True Accounting AI? Breaking the Rules-Based Paradigm

To successfully integrate artificial intelligence into an accounting practice, firm partners must distinguish between true AI and legacy rules-based automation. The market is saturated with software vendors appending “AI” to their product names, but the underlying architecture determines whether the tool will actually generate leverage for a firm.

The Limitations of Rules-Based Automation

For the last ten to fifteen years, accounting firms relied on strict rules-based macros to speed up bookkeeping. A firm would establish a hard-coded rule within the general ledger: “If the bank feed transaction contains the word ‘Delta,’ automatically code it to Travel Expense.”

While this was a step up from manual ten-key entry, it was profoundly fragile. Rules-based systems possess no contextual awareness.

If a client purchased advertising through a vendor whose newly altered legal name incidentally included the word “Delta,” the macro would blindly miscategorize the transaction. When clients switched payment processors, altered their vendor routing, or changed software protocols, these rigid connections severed immediately.

As a result, accounting professionals were frequently forced to operate as amateur IT technicians, spending days at the end of every month fixing broken bank-feed linkages and reversing hundreds of automated errors. Honestly, the system required constant, exhausting maintenance.

The Shift to Contextual Natural Language Processing

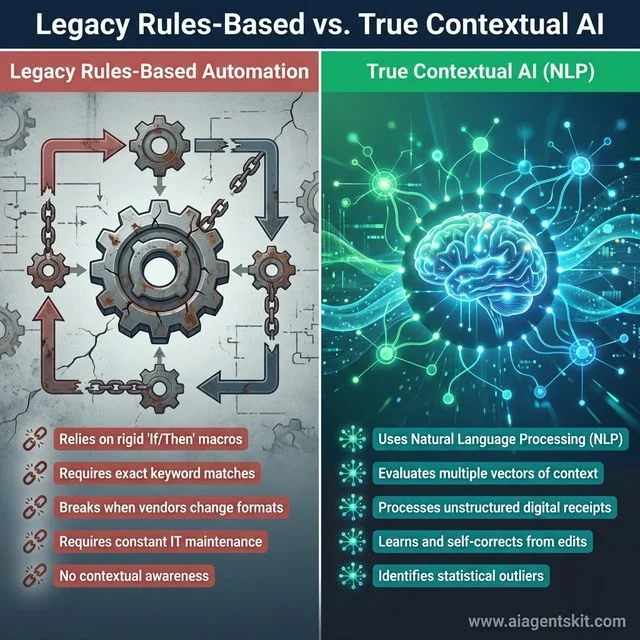

Legacy Rules-Based vs. True Contextual AI: A side-by-side comparison diagram illustrating the fundamental architectural shift in financial automation software. The left side (red) visualizes the fragility of legacy rules-based macros which rely entirely on rigid ‘If/Then’ Boolean logic, require exact keyword matches, break instantly when invoice formats change, and lack any contextual business awareness. The right side (green/blue) demonstrates the power of true contextual AI built on Natural Language Processing (NLP). Unlike brittle macros, advanced accounting AI evaluates multiple data vectors, processes entirely unstructured digital receipts without geometric templates, learns and self-corrects from user edits, and autonomously identifies complex statistical anomalies. This pivot from rigid automation to fluid machine learning allows modern CPAs to execute continuous close procedures without constantly repairing broken IT connections.

Legacy Rules-Based vs. True Contextual AI: A side-by-side comparison diagram illustrating the fundamental architectural shift in financial automation software. The left side (red) visualizes the fragility of legacy rules-based macros which rely entirely on rigid ‘If/Then’ Boolean logic, require exact keyword matches, break instantly when invoice formats change, and lack any contextual business awareness. The right side (green/blue) demonstrates the power of true contextual AI built on Natural Language Processing (NLP). Unlike brittle macros, advanced accounting AI evaluates multiple data vectors, processes entirely unstructured digital receipts without geometric templates, learns and self-corrects from user edits, and autonomously identifies complex statistical anomalies. This pivot from rigid automation to fluid machine learning allows modern CPAs to execute continuous close procedures without constantly repairing broken IT connections.

Modern accounting AI software operates on a fundamentally different structural paradigm. By using machine learning (ML), computer vision, and Natural Language Processing (NLP), true AI systems process financial documents contextually, much like a human accountant would.

Instead of relying on a brittle mapping rule, an AI agent evaluates multiple vectors of context. When analyzing a receipt or an invoice, the AI recognizes the vendor name, the total amount, the line items, the date, and the historical purchasing behavior of that specific client.

If it processes a $14 charge from “SBUX Store #4829” accompanied by an unstructured digital receipt, the NLP engine understands that this represents a business coffee meeting—not because it triggered a rigid rule, but because it recognizes the contextual pattern of the data.

Crucially, these intelligent software suites incorporate general accounting principles into their fundamental logic models. They flag statistical outliers for the controller’s review rather than automatically posting them.

Most importantly, machine learning systems continuously evolve. When a firm partner or senior CPA corrects a categorization suggested by the AI, the system updates its internal weighting protocol, ensuring that the same error is never repeated across the firm’s entire client portfolio.

This iterative, self-correcting evolution means the firm’s infrastructure literally grows more accurate and efficient with every passing month.

The Direct Impact of Artificial Intelligence on Accounting Firms

The overall impact of artificial intelligence on accounting firms extends far beyond simple bookkeeping automation. It is fundamentally reshaping how CPA firms structure their teams, interact with their clients, and scale their service offerings.

How AI is Changing the Accounting Industry

Historically, the success of a practice was tied to its ability to out-work the busy season via sheer manual effort. Today, how AI is changing the accounting industry involves a complete pivot from historical data recording to real-time predictive analysis.

Firm partners are finding that intelligent systems drastically reduce the time spent on mundane compliance tasks. This frees the human workforce to engage in much deeper, relationship-driven client advisory services.

Enhancing Accuracy and Reducing Liability

The immediate impact of AI on CPA firms is almost always felt in the substantial reduction of costly human error. By instantly cross-referencing thousands of ledger entries without fatigue, AI bookkeeping software benefits firms through mathematically flawless data sorting.

This level of continuous precision lowers the firm’s overall liability and provides a much cleaner audit trail during tax season. Ultimately, the true future of CPAs with AI implies becoming strategic verifiers of data rather than mechanical data entry clerks.

Scaling Operations Without Mass Hiring

Perhaps the most profound impact of artificial intelligence on the accounting sector is the ability to scale profits without scaling headcount. By aggressively adopting sophisticated AI accounting software, a boutique firm can comfortably handle the transaction volume of a much larger enterprise.

This technological leverage entirely changes the competitive landscape for small and mid-sized financial practices. It literally enables independent CPAs to punch far above their weight class and confidently acquire highly complex corporate clients using modern AI in finance tools.

The Death of the Billable Hour: A Necessary Evolution in Pricing Models

That said, bringing artificial intelligence into a CPA firm doesn’t merely change how the work is executed; it actively shatters the fundamental revenue model upon which most firms are built. For a century, the primary metric of firm profitability has been the billable hour.

Partners track time in six-minute increments, billing clients based on the duration required to manually draft returns, reconcile ledgers, and compile historical reports.

Artificial intelligence fundamentally disrupts the linear relationship between time and value.

The Efficiency Paradox

Consider a complex, multi-entity month-end close procedure that historically required forty billable hours from a mid-level accountant. If a firm successfully deploys advanced close-management AI, that same procedure might be executed in four hours of primarily review-based work.

If the firm continues to bill strictly by the hour, its reward for investing in enterprise AI, reducing client turnaround time, and improving general ledger accuracy is a 90% reduction in gross revenue for that client. This efficiency paradox terrifies veteran partners who have spent their entire careers equating hours directly to firm profitability.

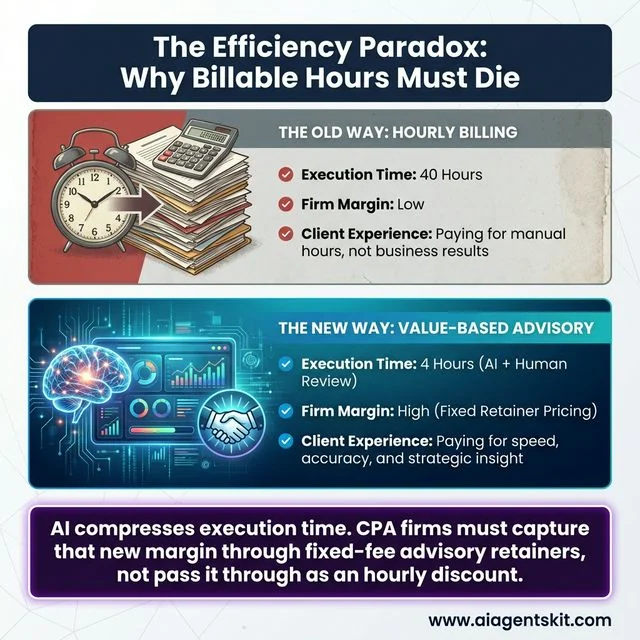

The Efficiency Paradox: Why Billable Hours Must Die: A visual comparison highlighting the necessity of transitioning from traditional hourly billing to fixed-fee value-based retainers. The top scenario depicts the outdated manual method where a month-end close requires 40 billable hours. While this historically generated high top-line revenue, it locked the firm into low-margin manual labor and penalized efficiency. The bottom scenario visualizes the modern hybrid approach where AI integration condenses the exact same close procedure down to just 4 hours of high-level strategic review. This creates an efficiency paradox where billing by the hour would severely reduce firm revenue. To capture the massive margin expansion generated by artificial intelligence, modern accounting practices must shift their pricing models to charge for strategic insight and accuracy rather than mere mechanical execution time.

The Efficiency Paradox: Why Billable Hours Must Die: A visual comparison highlighting the necessity of transitioning from traditional hourly billing to fixed-fee value-based retainers. The top scenario depicts the outdated manual method where a month-end close requires 40 billable hours. While this historically generated high top-line revenue, it locked the firm into low-margin manual labor and penalized efficiency. The bottom scenario visualizes the modern hybrid approach where AI integration condenses the exact same close procedure down to just 4 hours of high-level strategic review. This creates an efficiency paradox where billing by the hour would severely reduce firm revenue. To capture the massive margin expansion generated by artificial intelligence, modern accounting practices must shift their pricing models to charge for strategic insight and accuracy rather than mere mechanical execution time.

The Transition to Value-Based Advisory Pricing

To survive the integration of AI, accounting firms must transition from hourly billing to value-based pricing models. Clients don’t natively care how many hours it takes to compile a pristine balance sheet or execute a flawless tax return; they care about the accuracy, the strategic insight, and the peace of mind those deliverables provide.

Firms must shift to charging fixed monthly or annual advisory retainers. Under a value-based model, the firm agrees to provide continuous accounting, automated reconciliation, and forward-looking strategic advisory services for a set fee.

When AI deployment compresses the time required to execute the mechanical deliverables, the firm’s hourly realization rate skyrockets. The margin expansion created by AI is captured entirely by the firm, rather than passed through as a discount to the client.

This business model pivot requires extensive retraining for partners. They must learn to sell the value of their financial foresight—acting as fractional CFOs—rather than selling the manual labor of historical data aggregation.

I’m not entirely sure how fast the middle market will adapt, but the firms making the leap are seeing massive profit jumps.

6 High-Yield AI Workflows That Transform CPA Firms

When auditing a firm’s potential for technological upgrades, leadership must ignore flashy marketing promises and focus exclusively on specific, high-friction operational bottlenecks. AI should only be purchased to solve explicit workflow constraints.

The following six operational domains represent the highest-yield workflows where AI is currently delivering massive, quantifiable returns for modern accounting practices.

6 High-Yield AI Workflows for Accounting Firms: A grid layout displaying the specific domains where artificial intelligence delivers immediate, quantifiable return on investment. The workflows include Automated Client Onboarding for dynamic portal provisioning, Accounts Payable for contextual NLP extraction from unstructured vendor receipts, and Continuous Close for executing daily automated bank reconciliations aligned with accrual matching. It also highlights the Tax Prep Pipeline which autonomously parses disorganized client PDF dumps, Continuous Auditing which executes 100% comprehensive ledger scans to proactively detect fraudulent anomalies, and FP&A Forecasting which drives instant 3-way financial modeling for sensitivity analysis. By specifically targeting these distinct operational bottlenecks, firm leadership can safely integrate AI tools to systematically buy back thousands of hours of expensive human capital without resorting to overwhelming “rip-and-replace” software migrations.

6 High-Yield AI Workflows for Accounting Firms: A grid layout displaying the specific domains where artificial intelligence delivers immediate, quantifiable return on investment. The workflows include Automated Client Onboarding for dynamic portal provisioning, Accounts Payable for contextual NLP extraction from unstructured vendor receipts, and Continuous Close for executing daily automated bank reconciliations aligned with accrual matching. It also highlights the Tax Prep Pipeline which autonomously parses disorganized client PDF dumps, Continuous Auditing which executes 100% comprehensive ledger scans to proactively detect fraudulent anomalies, and FP&A Forecasting which drives instant 3-way financial modeling for sensitivity analysis. By specifically targeting these distinct operational bottlenecks, firm leadership can safely integrate AI tools to systematically buy back thousands of hours of expensive human capital without resorting to overwhelming “rip-and-replace” software migrations.

1. Automated Client Onboarding and Entity Setup

Client onboarding is historically a disjointed process of chasing emails, establishing secure folders, and manually configuring general ledgers. AI practice management tools now automate this entire sequence.

When a prospect signs an engagement letter, the AI triggers a cascading workflow. It automatically provisions the client portal, generates dynamic intake questionnaires based on entity type, and sets up preliminary chart of accounts mirroring similar clients in your firm’s database.

2. Accounts Payable & Pre-Accounting Ingestion

The manual processing of accounts payable is the lowest-hanging fruit for firm-wide automation. AP is historically high-touch, highly prone to human error, and tedious to manage across dozens of disparate clients.

Modern AP automation AI completely inverts this process.

When a vendor invoice arrives at the firm via email or client portal, an AI agent automatically intercepts the document. Using advanced computer vision combined with NLP, the system reads the invoice entirely free of geometric templates.

Even if a local contractor submits a highly unstructured, handwritten invoice that looks completely different from their previous submissions, the AI comprehends the contextual meaning of the text. The system instantly extracts the vendor entity, the invoice date, the due date, line-by-line descriptions, tax breakdowns, and the total amount due.

Beyond simple OCR extraction, the AI cross-references the newly ingested document against the client’s historical ledger to actively prevent duplicate payments. It then pre-populates the suggested expense categorization based on past firm-wide behavior.

The human accountant’s role fundamentally shifts from performing ten-key data entry to simply reviewing the AI’s drafted transaction and clicking “Approve.”

2. Continuous Month-End Close and Automated Bank Reconciliations

The traditional month-end close is an exhausting, compressed sprint that frequently takes anywhere from five to fifteen days to execute. The intense pressure of this period leads to high staff burnout and critically delays financial reporting delivery to business leadership.

AI shifts this delayed cycle into a continuous, rolling close. Specialized close management software uses integration APIs to connect directly to the client’s bank feeds, payroll providers, and corporate card systems.

Rather than piling vast amounts of reconciliation work into the first week of the new month, AI agents process standard transactions, accrual postings, and depreciation schedules in the background on a daily basis.

Furthermore, bank reconciliation AI doesn’t just look for identical numerical matches. If an invoice was raised for $5,000, but the bank feed registers a processed payment of $4,850 alongside a separate merchant processing fee of $150, the AI intelligently links those disparate data points, suggesting a unified reconciliation entry to balance the ledger.

By the time the calendar officially turns to the first of the month, the vast majority of the core close procedures are already finalized. In fact, Deloitte’s research on continuous accounting indicates that leveraging AI-driven close workflows can compress reporting cycles by up to 50%.

3. The Tax Preparation Pipeline and Document Parsing

Tax season represents the ultimate operational stress test for CPA firms, characterized by relentless hours, intense client demands, and high burnout rates. Adopting AI for tax preparation fundamentally alters the mechanics of this busy season.

Modern tax-focused AI is engineered to handle massive, chaotic influxes of client data. When a client uploads a disorganized PDF containing fifty pages of unsorted K-1s, W-2s, 1099s, and brokerage statements, the AI instantly separates, classifies, and renames the individual documents.

It then uses its NLP engine to extract the relevant financial figures and auto-populates those data points directly into the firm’s professional tax software.

Beyond mere mechanical data entry, advanced tax AI systems act as a secondary reviewer. The system can instantly cross-reference the client’s submitted documents against their previous year’s tax return, actively flagging missing information (e.g., “Client provided a 1099-B but is missing the corresponding cost basis statement”).

Additionally, some systems can constantly scan the drafted return against real-time updates to the federal tax code, surfacing missed deduction optimization opportunities and ensuring rigorous compliance before the partner even reviews the file.

4. Continuous Auditing and Fraud Detection

In traditional auditing frameworks, detecting fraud or errors relies heavily on “random sampling.” Human auditors manually review a statistically significant subset of a corporation’s transactions and extrapolate those findings to the entire ledger.

This method is inherently flawed, as subtle systemic errors often hide outside the randomly selected sample. According to the Association of Certified Fraud Examiners (ACFE), typical organizations lose 5% of their revenue to internal fraud each year due to these sampling gaps.

AI eliminates the necessity for sampling by executing a 100% comprehensive ledger scan in minutes. Acting as a tireless internal auditor, the AI can analyze the totality of millions of corporate transactions, instantaneously highlighting the exact microscopic anomalies that a human team would invariably miss.

The system flags highly suspicious behavioral patterns: vendor invoices that precisely match approval limits to bypass supervisor review, payments occurring at 3:00 AM on a Sunday, overlapping travel expenses submitted in different jurisdictions simultaneously, or a sudden spike in transactions with a newly onboarded vendor sharing a similar name to an established partner. This technological lever shifts the auditing paradigm from a retroactive, post-mortem sampling exercise to proactive, continuous fraud prevention.

5. AI-Assisted Tax Research and Advisory Scenario Planning

Navigating the US Internal Revenue Code is incredibly dense and historically required hours of manual research to build an advisory case. Specialized tools like Thomson Reuters’ Checkpoint Edge now utilize AI to assist with natural language tax research.

Instead of searching exact IRS section codes, a CPA can ask, “How do the new R&D capitalization rules under Section 174 specifically affect a software startup with remote international contractors?” The AI instantly surfaces the exact statutory language, summarizes the recent case law, and outlines the primary risks.

Furthermore, AI is being deployed for scenario planning during tax strategy meetings. If a client is considering a localized real estate 1031 exchange versus investing in a Qualified Opportunity Fund, AI modeling tools can instantly forecast the multi-decade tax implications of both scenarios based on the client’s current historical data.

6. Automated Financial Forecasting and FP&A

Traditional Financial Planning and Analysis (FP&A) relied on static Excel models that required constant manual updating and often broke when new variables were introduced. AI drastically improves fractional CFO services by automating predictive forecasting.

Platforms like Jirav and Fathom absorb a client’s historical general ledger data and automatically generate rolling 3-way financial models (Income, Balance, Cash Flow).

The AI can run instant sensitivity analyses: “If this SaaS client increases marketing spend by 15% but their customer churn rate also increases by 2%, exactly when will they breach their minimum cash reserve covenant?” This allows CPAs to present complex, real-time board packages that position them as indispensable strategic advisors rather than mere historians.

The 3 Foundational AI Tools for CPA Practices

The marketplace is currently flooded with software vendors aggressively rebranding their legacy products as “AI-powered” by simply adding a thin chatbot wrapper over old databases. Evaluating which tools deliver actual infrastructure-level automation is a daunting task for firm leadership.

Based on extensive real-world enterprise deployments, I highly recommend the following three tools as foundational pillars for a progressive, AI-driven CPA firm.

1. Vic.ai (The Pre-Accounting and AP Engine)

Best for: Autonomous invoice processing and enterprise-grade accounts payable.

Vic.ai operates almost exclusively in the pre-accounting and accounts payable domain, and it remains the industry gold standard for ingestion automation. Unlike early-generation OCR software that required firms to painstakingly draw boundary boxes and build rigid spatial templates for every unique vendor, Vic.ai’s advanced computer vision models understand invoices globally out of the box.

Because the platform has been trained on hundreds of millions of invoices across thousands of companies, its Day-One accuracy is astonishingly high. It natively learns the firm’s specific general ledger coding preferences and routing protocols rapidly.

If a firm is currently drowning in the administrative overhead of tracking down vendor invoices, attempting to match complex purchase orders, and manually typing line items into an ERP, deploying Vic.ai entirely removes human staff from the foundational data entry loop.

2. Botkeeper (The Hybrid Bookkeeping Manager)

Best for: Outsourced, scalable GL management and continuous reconciliation.

Botkeeper takes a highly pragmatic, deeply effective approach to accounting automation by offering “automated bookkeeping support” through a hybrid model. The platform uses proprietary machine learning algorithms to handle the vast majority of routine transaction categorization, bank feed management, and standard monthly reconciliations.

However, Botkeeper acknowledges the current limitations of artificial intelligence. When the AI encounters an unprecedented edge-case transaction that it cannot resolve with an exceptionally high degree of confidence, the system automatically routes the transaction to Botkeeper’s internal team of human accounting engineers.

This “Human-in-the-loop” failsafe ensures that errors don’t compound silently in the background. For CPA firms attempting to scale their outsourced accounting or Client Advisory Services (CAS) divisions without hiring an army of expensive onshore bookkeeping staff, Botkeeper serves as a massive operational lever.

3. TaxDome (The Tax Practice Operating System)

Best for: Practice management, document routing, and tax season workflow autonomy.

TaxDome serves as the central nervous system for tax-heavy accounting practices. While it functions as a comprehensive client portal and CRM, TaxDome has aggressively integrated deep AI into its document management and workflow automation pipelines.

When clients dump unorganized tax documents into the secure portal, TaxDome’s AI automatically recognizes the document type, renames the file according to the firm’s strict internal naming conventions, routes it to the correct secure folder, and automatically initiates the corresponding tax prep workflow for the designated staff member. Furthermore, it uses AI to trigger conditional email follow-ups to clients who have failed to submit required identification or signature sheets.

If a firm’s primary operational bottleneck is the sheer administrative chaos of tracking client documents from January to April, TaxDome’s integrated AI routing resolves the core communication breakdown.

(Note: For firms dealing heavily in corporate spend management, using platforms like Ramp and Numeric can provide similarly profound leverage for automated GL synchronization and sophisticated close management tracking. Read more about deploying these tools in our guide to the growing SMB software stack.)

Data Security Governance: Navigating SOC 2 and the Human-in-the-Loop Imperative

As firms rush to aggressively adopt artificial intelligence, a critical, potentially catastrophic vulnerability is emerging across the industry. I’ve literally seen firm partners bypass official IT governance, driven by a desire for fast efficiency.

The Danger of Public Large Language Models

There is a disturbing trend of well-intentioned accountants copying raw, unanonymized client financial spreadsheets and pasting them directly into the public, consumer-grade versions of models like ChatGPT, Claude, or Gemini to request rapid variance analysis or summary reporting.

Honestly, this practice represents a severe breach of data security protocols. When client data is submitted into a consumer-grade public AI model, the firm is frequently agreeing to Terms of Service that permit the AI corporation to use that specific data to train future iterations of their public models.

This constitutes a direct breach of client confidentiality, and directly violates the American Institute of CPAs (AICPA) privacy guidelines. It also exposes the firm to massive liability under rigid data governance laws such as GDPR or CCPA.

Enterprise Safeguards and SOC 2 Type II Compliance

If an accounting firm intends to adopt AI, leadership must mandate the use of closed, enterprise-grade environments. The foundational tools implemented by the firm—such as Botkeeper or Vic.ai—must maintain explicit, verifiable SOC 2 Type II compliance.

Enterprise AI platforms function within highly isolated, single-tenant environments. The data ingested into these systems is rigorously fenced; it’s never aggregated or used to train the broader public baseline models.

Firm leadership must demand explicit data privacy guarantees, zero-retention policies, and comprehensive penetration test summaries from any third-party AI software vendor before integration. In 2026, ignorance regarding software data pipelines is not a legally defensible position in the event of a client breach.

The Explainability Mandate

Another critical compliance factor specific to the accounting industry is the concept of algorithmic explainability. When an external auditor or regulatory body questions why a specific, complex journal entry was executed, responding that “the artificial intelligence generated it” is entirely insufficient.

True enterprise accounting AI maintains a rigid, immutable audit trail. The software must clearly document the unbroken cryptographic lineage linking the AI’s generated journal entry directly back to the original source document, explicitly state the internal logic or historical precedent the AI applied to make its determination, and permanently record the digital signature of the human accountant who ultimately reviewed and authorized the execution.

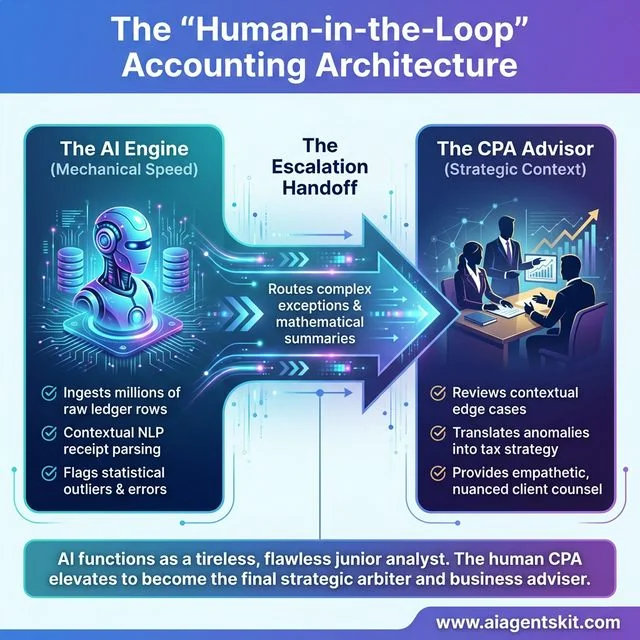

The Human-in-the-Loop Architecture

This explainability mandate underlines why artificial intelligence won’t fundamentally replace Certified Public Accountants. In my experience, the industry is permanently shifting toward a “Human-in-the-Loop” architecture.

In this model, the AI functions as a tireless, mathematically flawless junior staff member traversing millions of data points, executing initial ingestion, parsing, and draft coding at light speed. However, the human CPA elevates to the critical role of the final strategic reviewer and contextual arbiter.

The accountant no longer verifies the fundamental arithmetic; they verify the broader business context. If the AI flags a sudden, drastic variance in quarterly R&D spend, the CPA doesn’t merely approve the math—they use that insight to immediately contact the client, discuss shifting tax optimization strategies regarding Section 174 capitalization, and provide top-tier advisory council.

The Human-in-the-Loop Accounting Architecture: A workflow diagram demonstrating the secure and optimal deployment of AI within a CPA practice. The sequence begins on the left with the AI Engine utilizing its massive mechanical speed to ingest millions of raw ledger rows, execute contextual NLP parsing of unstructured documents, and instantaneously flag statistical outliers. Following the escalation handoff, the process routing forwards these complex mathematical summaries to the human professional. On the right, the CPA Advisor applies deep strategic context—reviewing edge cases, translating data anomalies into proactive tax strategy, and providing the empathetic, nuanced business counsel that algorithms cannot replicate. In this paradigm, artificial intelligence acts as a mathematically flawless junior analyst, allowing the human accountant to elevate entirely into the role of independent strategic arbiter.

The Human-in-the-Loop Accounting Architecture: A workflow diagram demonstrating the secure and optimal deployment of AI within a CPA practice. The sequence begins on the left with the AI Engine utilizing its massive mechanical speed to ingest millions of raw ledger rows, execute contextual NLP parsing of unstructured documents, and instantaneously flag statistical outliers. Following the escalation handoff, the process routing forwards these complex mathematical summaries to the human professional. On the right, the CPA Advisor applies deep strategic context—reviewing edge cases, translating data anomalies into proactive tax strategy, and providing the empathetic, nuanced business counsel that algorithms cannot replicate. In this paradigm, artificial intelligence acts as a mathematically flawless junior analyst, allowing the human accountant to elevate entirely into the role of independent strategic arbiter.

Actionable AI Prompts for Firm Leadership and Advisory Services

While consumer-grade LLMs (like the standard web interface of ChatGPT) pose security risks when handling raw financial ledgers, they remain powerful tools for firm leadership when deployed safely. Firm partners can safely deploy public LLMs for non-PII (Personally Identifiable Information) tasks to drastically increase their communication speed, generate complex formulas, and scale their advisory presence.

The key to safe utilization is aggressive abstraction: keeping specific client names, proprietary numbers, and identifiable business details entirely out of the prompt window.

Here are six actionable, high-leverage ways firm leadership can use safe AI prompts in their daily workflows today:

1. Scaling Client Advisory Communication

Partners spend hours drafting bespoke emails explaining complex regulatory changes to anxious clients. AI can reduce a 30-minute drafting process to 30 seconds.

- The Safe Prompt: “I am the managing partner of a CPA firm. Next week, I need to send an email blast to my small business clients regarding the updated IRS thresholds for 1099-K reporting and how it impacts their ecommerce sales. Draft a professional, reassuring 4-paragraph email explaining the compliance changes. Write it at an 8th-grade reading level, aggressively remove all deep tax jargon, and include three bulleted action items they need to take before Q3. Maintain a tone that positions our firm as their proactive, protective partner.”

2. Rapid Formula and Macro Generation

Advanced data manipulation often requires exceptionally complex Excel formulas, VBA macros, or Google Sheets scripts that accountants either have to painstakingly build or search forums to solve.

- The Safe Prompt: “I am building a comprehensive cash flow forecasting model in Excel. I have a dynamically updating list of projected vendor payment dates in Column A, and the corresponding payment amounts in Column B. Write an advanced Excel formula (do not use VBA) that looks at the current date, and sums only the payments that are scheduled to fall on a weekend over the next 45 days, so I can adjust the treasury sweep schedule. Provide a brief explanation of how the formula works so I can audit it.”

3. Creating Internal Firm Policy and Change Management Documents

As firms adopt new technology, creating the internal governance documentation can be a massive administrative burden for leadership.

- The Safe Prompt: “I am a partner at a mid-sized accounting firm. We are deploying a new AI-driven accounts payable software next month. Draft a comprehensive ‘Internal AI Software Acceptable Use Policy’ for our junior accounting staff. Include strict sections prohibiting the uploading of client PII to unapproved public LLMs, guidelines on verifying AI-drafted journal entries before approval, and a protocol for escalating unexpected AI categorizations to management. Structure it with clear headings and a mandatory signature block at the end.”

4. Drafting Difficult or Awkward Client Conversations

Every CPA knows the dread of sending the “fee increase” email or telling a client they are missing a critical deadline because they didn’t provide documentation on time. AI is exceptional at softening the blow while maintaining professional boundaries.

- The Safe Prompt: “I am a CPA. I need to write an email to a long-term, slightly demanding client. They have consistently delivered their tax documents three weeks late, causing my staff to work weekends. I need to inform them that moving forward, we are instituting a firm 30-day cutoff rule before the final deadline, otherwise they will be automatically put on extension. Draft a polite but extremely firm email that protects our boundaries without ruining the relationship.”

5. Demystifying Dense Regulatory Updates (FASB/GAAP)

When the Financial Accounting Standards Board drops a 300-page update on lease accounting or revenue recognition, no one actually wants to read it cover-to-cover. AI can act as a high-level summarization engine.

- The Safe Prompt: “Act as a technical accounting researcher. Summarize the core changes made in the latest FASB ASU [insert specific ASU number] regarding debt issuance costs. Give me the top 3 bullet points on how this fundamentally changes the reporting requirements on the balance sheet for a mid-market manufacturing company. Keep it concise and reference the specific paragraph numbers if possible.”

6. Brainstorming Tax Optimization Strategies (Without PII)

If a partner is staring at a blank whiteboard trying to map out a complex strategy for a new client niche, AI can serve as a robust brainstorming partner to ensure no stone is left unturned.

- The Safe Prompt: “I am advising a high-net-worth client who recently sold a highly appreciated commercial real estate asset. Provide a bulleted list of 5 common, legally established tax deferral or optimization strategies (such as 1031 exchanges, Opportunity Zones, etc.) that I should review before our advisory meeting. Only provide strategies established within the current US tax code. I am asking for brainstorming purposes only, not legal advice.”

💡 3 Practical Tips for CPAs Using Conversational AI

If your firm is just beginning to experiment with tools like ChatGPT or Claude, follow these three rules to ensure massive utility without risking your reputation:

- Enforce the ‘No Number’ Rule: Train your staff that public AI models are strictly for words, structures, and concepts, not for calculations. If a prompt contains actual dollar figures or social security numbers, it’s a catastrophic breach of protocol.

- Use Persona Framing: AI models perform drastically better when you assign them a specific role. Always start your prompt with phrases like, “Act as a tough IRS auditor…” or “Act as an empathetic CFO for a tech startup…” This constrains the AI’s tone and prevents generic, robotic outputs.

- Mandate the ‘Rule of Review’: AI is highly persuasive even when fabricating information entirely. Treat the AI exactly like an eager but reckless intern. Every assertion, cited tax code, or drafted email must be reviewed and verified by a human professional before it leaves the firm.

By employing AI for high-level communication and structural drafting while strictly excluding proprietary data, partners harness the profound linguistic power of these models without triggering security compliance failures.

Change Management: Implementing AI Without Breaking Your Firm

A common fallacy among accounting firm leadership is the belief that purchasing modern software instantly results in operational efficiency. In reality, reading about artificial intelligence is easy; fundamentally rewiring a firm’s entrenched daily habits is brutally difficult.

Attempting to execute a “rip and replace” of a firm’s entire legacy software stack over a single weekend invariably ends in absolute operational disaster, frustrated staff, and panicked clients. To successfully deploy these transformative tools, partners must execute a controlled, phased change management protocol.

Step 1: Execute a Granular Bottleneck Audit

Leadership must not purchase software simply searching for a problem to solve. Before evaluating any vendors, partners should conduct a granular operational audit.

Where exactly are the most billable hours bleeding? Are staff spending twenty hours a week relentlessly chasing uncooperative clients for missing receipts? Is the firm consistently missing internal deadlines due to spreadsheet crashes during month-end close?

Leadership must identify the single most painful operational constraint before proceeding.

Step 2: Select a Single, Specialized Tool

Once the primary bottleneck is identified, the firm must select one specific, best-in-class tool to aggressively attack that exact problem. If accounts payable is the nightmare, the firm should implement Vic.ai.

Leadership should absolutely avoid the temptation to implement AP automation, sophisticated predictive forecasting, and AI-driven lease compliance software simultaneously. Staff require dedicated time to adapt their cognitive workflows to rely on automated systems.

Step 3: Mandate Shadow Parallel Testing

Never execute a blind switchover. For the initial thirty to sixty days, the firm must run the newly deployed AI system entirely in parallel with the legacy manual process.

The AI system should ingest the data and draft the entries, while a human staff member executes the identical localized task in the legacy system.

This parallel testing phase serves two critical purposes. First, it allows leadership to objectively quantify the AI’s accuracy rate in their specific operating environment. Second, and vastly more important, it builds vital psychological trust among the staff.

Veteran accountants will naturally resist artificial intelligence if they don’t trust its output. Allowing them to physically witness the AI flawlessly categorize sixty complex invoices in twelve seconds is the only effective method for overcoming professional skepticism.

Unlocking this trust allows the firm to eventually rely on the software to start cutting administrative time at scale.

Step 4: Redefining KPIs to Match AI Velocity

As detailed previously in the billing models section, AI destroys the traditional logic of the billable hour. If a firm successfully implements these systems, junior staff will finalize their workloads much faster.

If leadership evaluates those staff members based on total hours billed, the staff will be actively penalized for the firm’s technological efficiency.

The success of a firm-wide AI implementation requires partners to fundamentally redefine how they measure employee value. Key Performance Indicators (KPIs) must immediately pivot away from hours billed and toward metrics that reflect actual client value delivery.

Staff should be evaluated on the total volume of clients managed, the measurable reduction in general ledger error rates, client retention velocity, and the proactive advisory insights they generate.

The Future of the CPA Advisory Role

The transition to artificial intelligence within the accounting profession is not a theoretical scenario plotted for the next decade; it is the concrete, unavoidable operational baseline of 2026. The era of treating vast lakes of financial data as a manual, retroactive chore is permanently over.

By systematically adopting specialized accounting ai software to handle accounts payable ingestion, bank feed reconciliations, and tax document parsing, progressive firm leadership can buy back thousands of hours of expensive human capital. However, the ultimate objective of this transition is not merely to execute the exact same mechanical work at a slightly faster pace with fewer people.

The true strategic mandate is to weaponize that newly freed operational capacity. Firms must use their human talent to deliver the high-margin, forward-looking strategic counsel that modern business clients desperately require in a volatile, rapidly shifting economic climate.

The CPA firms that aggressively adopt this hybrid operational model will dominate their markets, while those who cling to manual data entry and strictly hourly billing will find themselves quickly rendered economically obsolete.

Frequently Asked Questions

What is the best AI accounting software for CPA firms?

There is no single monolithic “best” tool, as the optimal solution depends entirely on the firm’s most critical operational bottleneck. For deep accounts payable automation and autonomous invoice ingestion, Vic.ai is a market leader due to its sophisticated, template-free computer vision models.

For highly scalable outsourced hybrid bookkeeping, Botkeeper excels because it seamlessly balances automated ML processes with a robust human-in-the-loop oversight team. For complex tech startups and multi-entity organizations requiring advanced revenue recognition, Rillet is powerful because it natively understands developer-centric business models.

Successful firms build specialized, modular tech stacks via API integrations rather than relying on massive, slow-moving legacy suites.

How is AI going to impact the accounting profession structurally?

AI is commoditizing foundational bookkeeping, data ingestion, and routine report generation. The structural impact is a massive, industry-wide acceleration away from historical compliance reporting and toward proactive, forward-looking advisory services.

CPA firms will effectively manage larger client portfolios using smaller, highly strategic teams that deeply rely on AI infrastructure to process raw data. The accounting professionals who dominate the next decade won’t necessarily possess the strongest mechanical math skills; they’ll possess superior communication and strategic skills, specifically the ability to translate AI-generated predictive dashboards into actionable, empathetic business advice for stressed corporate founders.

Will AI replace accountants and CPAs entirely?

No. Artificial intelligence replaces mechanical tasks, not complex professionals. Modern software vastly outperforms humans at anomaly detection, rapid data categorization, and high-volume data extraction.

However, AI software completely lacks contextual business judgment, human empathy, and the nuanced capability to negotiate aggressive terms with a bank or advise a founder on the psychological ramifications of a hostile acquisition. If a client is navigating a devastating divorce that fragments the ownership of their holding company, an AI agent cannot navigate the deeply emotional and strategic nuances required to facilitate that asset division.

CPAs who refuse to adopt AI will inevitably be replaced by CPAs who do. The technology functions as a profound operational lever, not a wholesale replacement.

What exactly is the difference between legacy OCR and modern AI ingestion?

Legacy OCR (Optical Character Recognition) was fundamentally rigid and geometric. A software administrator had to draw specific boundary boxes on a digital template and instruct the software, “The total invoice amount is always located inside this specific coordinate box.”

If a vendor merely redesigned their invoice template, the OCR rule failed catastrophically. Modern AI uses a combination of advanced OCR and Natural Language Processing (NLP) to read the document contextually, much like a human does.

Regardless of the layout—even if a local contractor hastily hand-writes an invoice on a notebook page—the AI comprehends the contextual meaning behind the terms “Balance Due” or “Total” and correctly extracts the precise integer without requiring any pre-established template training. It parses semantic meaning, not arbitrary geometry.

How does AI transform the month-end close procedure?

Modern accounting AI software automates the month-end close by transforming it from a compressed, high-stress, end-of-period sprint into a truly continuous daily process. Rather than waiting until the final day of the month to begin aggregating data, AI systems continuously reconcile live bank feeds, automatically pull in expense reports via active API integrations with corporate cards, parse incoming vendor invoices via NLP, and track missing client documentation instantaneously.

By deploying intelligent pattern matching to pre-approve routine entries, the AI handles the vast majority of the bulk data workload throughout the month. When the period ends, the CFO or Controller is merely left to review flagged anomalies and approve final automated accruals, reducing the close cycle from weeks to a matter of days.

How much does enterprise AI accounting software typically cost a firm?

Implementation costs vary wildly based on the firm’s specific scale, total entity count, and overall transaction volume. Some modern corporate expense management platforms, such as Ramp, offer their highly sophisticated core AI receipt-parsing features essentially for free (as their revenue model relies on merchant interchange fees).

Conversely, standalone enterprise AP automation or specialized continuous close management software can range from several hundred to several thousand dollars per month. While a $3,000 monthly software subscription might induce initial sticker shock for a managing partner, it must be accurately measured against the fully loaded cost—including salary, benefits, and training—of multiple junior accountants.

If the software immediately eliminates the need for two full-time hires while exponentially increasing tracking accuracy and reporting speed, the Return on Investment (ROI) is generally realized within the first ninety days of deployment.

If your firm is ready to explore immediate ways to begin modernizing its underlying practice architecture, dive deeply into our comprehensive AI implementation roadmap to start reclaiming your firm’s administrative time today.

If you work with law firm clients or run a legal practice alongside accounting services, our companion post on AI for law firm management covers the same operational transformation across the legal vertical — with specific tools for legal research, client intake, and billing model evolution.

Accounting firms that also serve real estate clients — investors, developers, brokerages — will find the complete AI stack guide for real estate agencies directly applicable: the same CRM automation, document processing, and operational AI layers covered here have direct parallels in how real estate organizations are restructuring their workflows.